Insurance Themes: Navigating the AI Capex Boom

Senior Vice President, Head of Insurance Portfolio Management

Senior Insurance Portfolio Manager

Key Takeaways

Navigating the AI credit glut: A staggering amount of AI capex debt is coming to market across public corporate bonds, private credit, and securitized products. For insurance investors, novel structures demand careful security selection as well as a holistic view of overall portfolio concentration risk given the size and breadth of funding.

Tracking the regulator’s next move: With new CLO capital charges in place, many insurers are wondering what’s next on the NAIC’s agenda. Our bet is ABS in the near term, with RNFs a longer-term challenge.

Taking the Fed’s temperature: It was easier to discount rising inflation when it was due to exogenous shocks like the Iran war. But a reacceleration in the labor market means Warsh must walk a fine line to appease both the hawks on the FOMC and doves in the White House.

AI-related debt is now over 15% of the U.S. investment grade bond universe and responsible for multiple $10+ billion private placements, and that’s not even taking into account associated sectors such as power generation. Here’s where we see potential—and pitfalls—for insurance allocations.

Digesting data center debt

One of the most persistent discussions in markets over the past few years has been whether U.S. equity markets are too concentrated. At present, AI-related companies represent around 49% of the S&P 500, and significant non-index AI names have either recently IPOed (SpaceX) or have filed for IPO (Anthropic; OpenAI).1

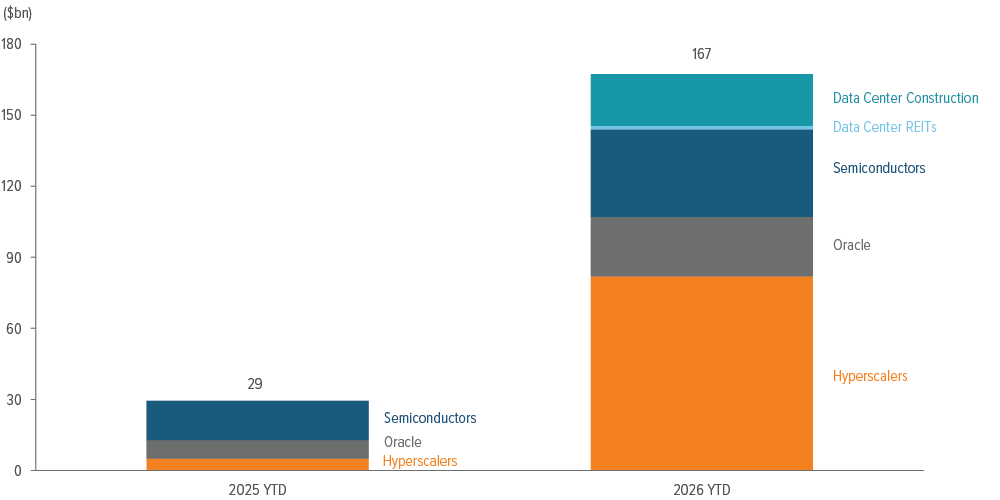

Mega-deals from AI hyperscalers in late 2025 brought that theme to the fore in debt markets, too (Exhibit 1). AI-related issuance is already over 15% of the investment grade (IG) bond market, and forecasts for total AI-related debt issuance in 2026 top out at over half a trillion dollars.2

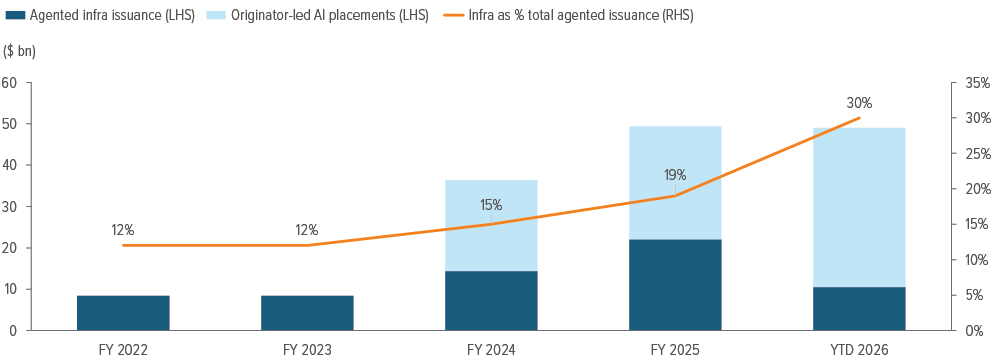

The story is much the same in the investment grade private placement market, which is seeing a raft of mega-placements from non-bank originators (Exhibit 2).

As of 06/15/26. Source: Bloomberg.

The sheer size of the funding need for the AI buildout, estimated at $5.5 trillion, means that issuers will need to tap every channel to mitigate costs of capital and investor fatigue in capital markets.3

The first, and obvious, impact of the AI debt-a-palooza is an increasing need for insurers to look at portfolios holistically to mitigate the risk of over-exposure to any one name. At this point an insurer could theoretically hold an equity stake in Meta while also owning Meta bonds, its data center private placement, and its GPU financing—exposure that could be unknowingly spread out across four different investment teams or mandates.

The second impact is the necessity of evaluating the fine print of a deluge of seemingly similar transactions across multiple debt markets with an eye towards mitigating downside risk and maximizing relative value.

Structures are novel and heterogenous in nature, so security selection is key to avoid embedded risks like extension and lease termination, especially for cutting edge technology that could face obsolescence risk in the future. Where should insurance investors allocate their AI debt dollars?

As of 6/15/26. Source: BofA, Voya Investment Management. “Agented” issuance represents investment bank-led infrastructure placements, not all of which are AI or data center related. “Originator-led” issuance includes both Reg D and Rule 144A placements executed primarily by non-bank originators, such as the Beignet Investor (Meta) placement in 2025. Agented data is only to end 1Q 2026; originator-led data is to 06/15/26.

A note about risk

The principal risks are generally those attributable to bond investing. All investments in bonds are subject to market risks as well as issuer, credit, prepayment, extension, and other risks. The value of an investment is not guaranteed and will fluctuate. Market risk is the risk that securities may decline in value due to factors affecting the securities markets or particular industries. Bonds have fixed principal and return if held to maturity but may fluctuate in the interim. Generally, when interest rates rise, bond prices fall. Bonds with longer maturities tend to be more sensitive to changes in interest rates. Issuer risk is the risk that the value of a security may decline for reasons specific to the issuer, such as changes in its financial condition. High yield securities, or “junk bonds,” are rated lower than investment grade bonds because there is a greater possibility that the issuer may be unable to make interest and principal payments on those securities. Foreign investing does pose special risks, including currency fluctuation, economic and political risks not found in investments that are solely domestic. Emerging market securities may be especially volatile. Investments in mortgage-related securities involve exposure to prepayment and extension risks greater than investments in other fixed income securities. The strategy may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and could have a potentially large impact on performance. Investments in commercial mortgages involve significant risks, which include certain consequences that may result from, among other factors, borrower defaults, fluctuations in interest rates, declines in real estate values, declines in local rental or occupancy rates, changing conditions in the mortgage market, and other exogenous economic variables. All security transactions involve substantial risk of loss. The strategy will invest in illiquid securities and derivatives and may employ a variety of investment techniques, such as using leverage and concentrating primarily in commercial mortgage sectors, each of which involves special investment and risk considerations. Other risks include, but are not limited to: credit risks; credit default swaps; currency; interest in loans; liquidity; other investment companies’ risks; price volatility risks; inability to sell securities risks; U.S. government securities and obligations; sovereign debt; and securities lending risks.