Fixed Income: Navigating the AI Capex Boom

Head of Multi-Sector Fixed Income

Senior Vice President, Head of Asset-Based Finance

Senior Vice President, Head of Infrastructure

AI-related debt is now over 15% of the U.S. investment grade bond universe and responsible for multiple $10+ billion private placements, and that’s not even taking into account associated sectors. Here’s where we see potential— and pitfalls—for fixed income portfolios.

Key takeaways

- AI capex is driving a once-in-a-cycle fixed income supply shock, with AI-related debt now a meaningful share of both public and private investment grade (IG) issuance.

- This dynamic makes cross-portfolio risk management and disciplined structure selection more necessary than ever.

- In a market of ever-expanding and often untested structures, we see the best relative value in a barbell strategy of shorter-dated private placements and longdated public IG bonds.

- Private placements in GPU financing, construction finance, and other ABF deals stand out as offering both alpha and risk control.

- Public IG hyperscaler bonds provide duration and revenue diversification on the long end, while IG data center project bonds add spread.

Digesting data center debt

One of the most persistent discussions in markets over the past few years has been whether U.S. equity markets are too concentrated. At present, AI-related companies represent around 49% of the S&P 500’s market cap, and significant non-index AI names have either recently IPOed (SpaceX) or have filed for IPO (Anthropic; OpenAI).1

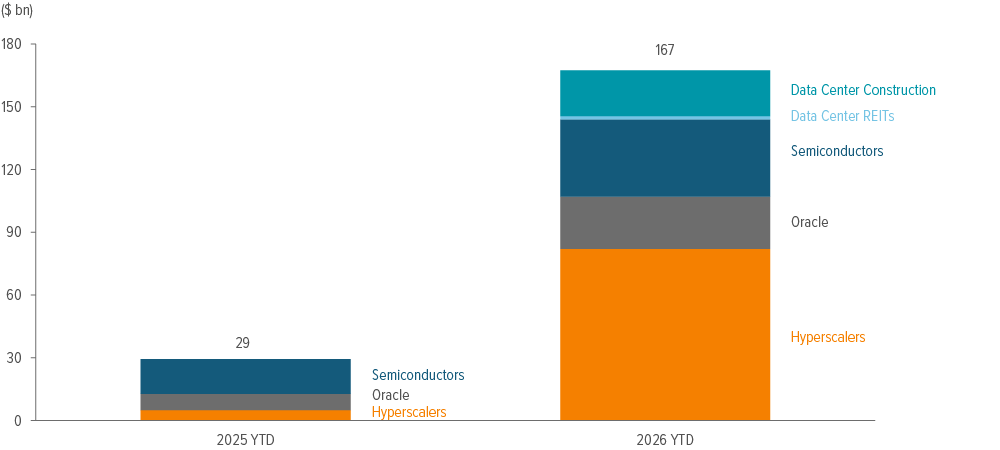

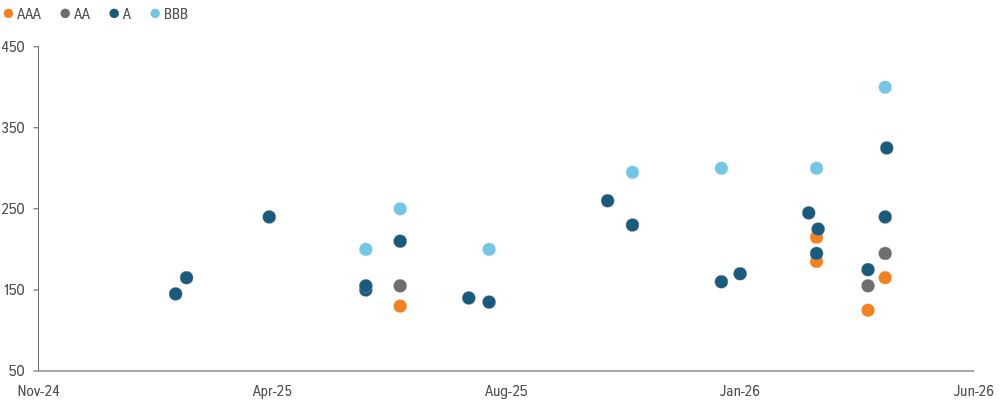

Mega-deals from AI hyperscalers in late 2025 brought that theme to the fore in debt markets, too (Exhibit 1). AI-related issuance is already over 15% of the investment grade (IG) bond market, and forecasts for total AI-related debt issuance in 2026 top out at over half a trillion dollars.2

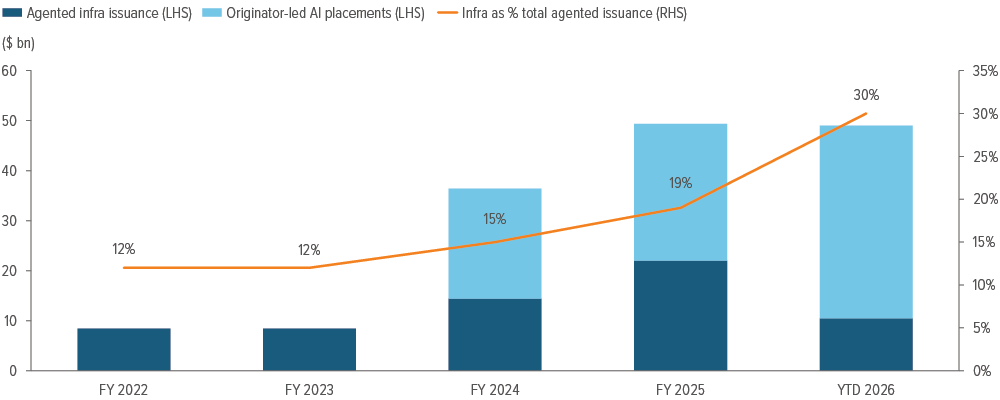

The story is much the same in the investment grade private placement market, which is seeing a raft of mega-placements from non-bank originators (Exhibit 2).

As of 06/15/26. Source: Bloomberg.

The sheer size of the funding need for the AI buildout, estimated at $5.5 trillion, means that issuers will need to tap every channel to mitigate costs of capital and investor fatigue in capital markets (Exhibit 4).3

The first, and obvious, impact of the AI debt-a-palooza is an increasing need for investors to look at portfolios holistically to mitigate the risk of over-exposure to any one name. At this point an investor could theoretically hold an equity stake in Meta while also owning Meta bonds, its data center private placement, and its GPU financing—exposure that could be unknowingly spread out across four different investment teams or mandates.

The second impact is the necessity of evaluating the fine print of a deluge of seemingly similar transactions across multiple debt markets with an eye towards mitigating downside risk and maximizing relative value.

Structures are novel and heterogenous in nature, so security selection is key to avoid embedded risks like extension and lease termination, especially for cutting edge technology that could face obsolescence risk in the future.

As of 06/15/26. Source: BofA, Voya Investment Management. “Agented” issuance represents investment bank-led infrastructure placements, not all of which are AI or data center related. “Originator-led” issuance includes both Reg D and Rule 144A placements executed primarily by non-bank originators, such as the Beignet Investor (Meta) placement in 2025. Agented data is only to end 1Q 2026; originator-led data is to 06/15/26.

Where should investors allocate their AI debt dollars?

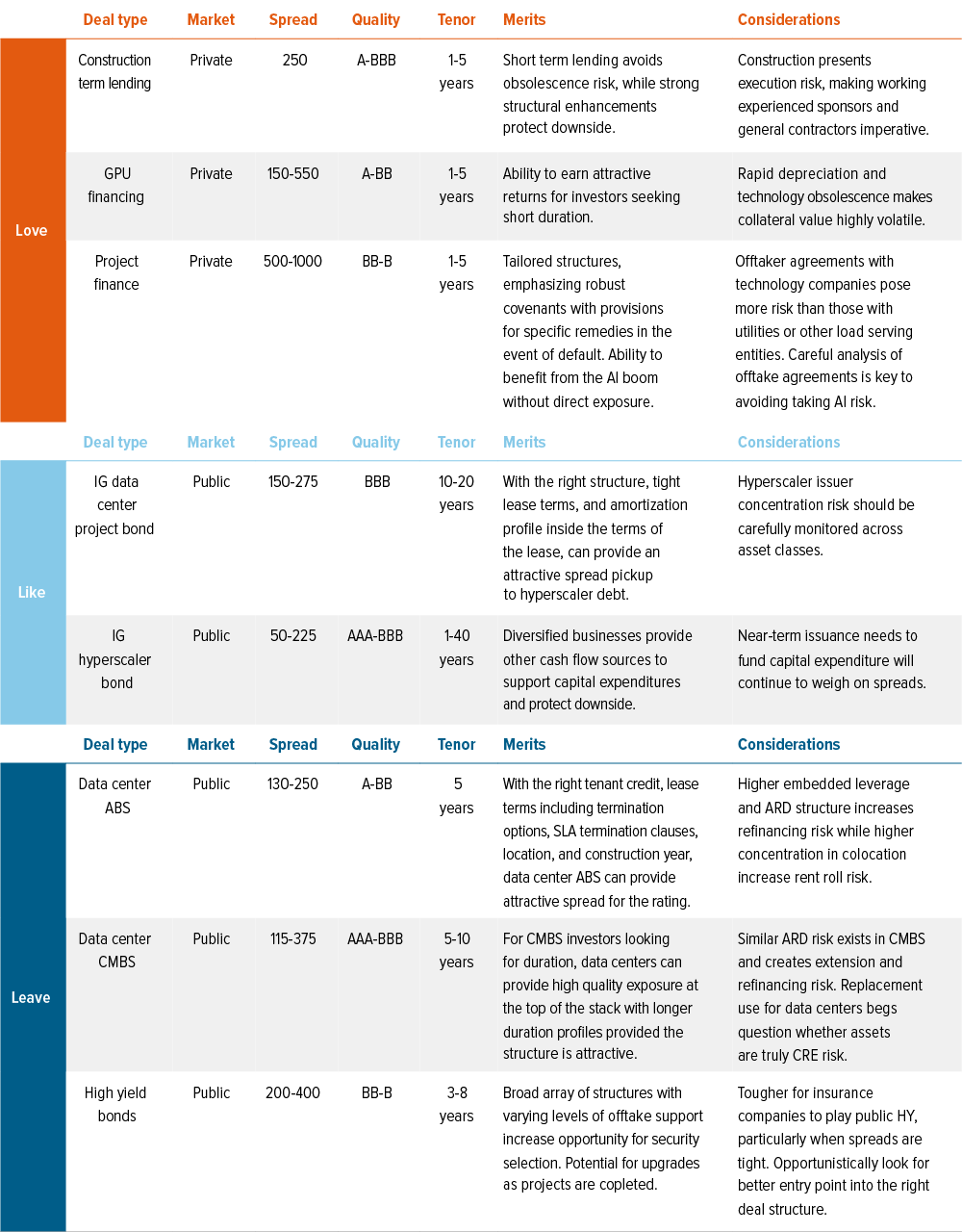

Across the broad (and continually broadening) opportunity set to invest in AI and hyperscalers, we believe superior relative value is offered in well-structured private placements, followed by investment grade corporate bonds (Exhibit 3).

Pairing these exposures enables a barbell approach, with shorter deals that are insulated from obsolescence risk balancing longer duration exposure to hyperscalers that have diversified businesses and cash flow sources away from AI.

While it is nearly impossible to get away from equity-market holdings in big tech companies, increasing concentration risk means the traditional large cap equity index exposures should be reevaluated to maintain diversification discipline.

As of 06/18/26. Source: Voya IM.

As of 06/15/26. Source: Bloomberg; Voya IM.

Longer-duration AI debt: Choose carefully, stick with quality

Most of the longer-dated AI-related private placements have been to fund data center projects. How you look at the risks associated with building out data centers comes down to whether you think they behave like true commercial real estate—or not.

This has been one of the most hotly-debated subjects on our desk. Ultimately we have come down to the belief that data centers fall somewhere uncomfortably in between commercial real estate and infrastructure. For one, their cost per square foot is wildly, incandescently higher than that of any other form of commercial real estate—which has caused our commercial mortgage loan team to steer clear of them.

And then there is the reuse question. If overall demand drops off for data centers, what tenant moves in there? Increasingly, data centers are being sited in the middle of nowhere because of community pushback—nobody wants them in their backyard. That type of isolated location can make it difficult for the building to be modified for a different type of tenant.

It’s hard not to see a hint of the late-1990s telecom boom, and this has influenced our thinking in a few ways.

The first is that we are wary of both refinancing risk and leasing risk. On the investment grade private placement side, that means we are looking for amortizing deals from strong sponsors that fully repay before any lease renewal happens.

For the lease term covered by the placement, we are looking for a high-quality, investment-grade tenant who is unable to cancel or otherwise get out of their lease contract before the placement repays.

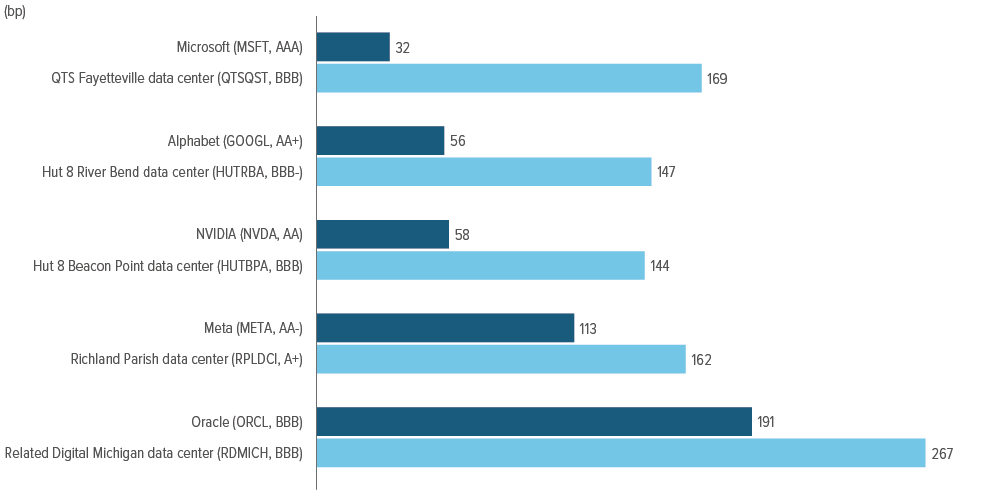

Data center project bonds vs. hyperscaler bonds

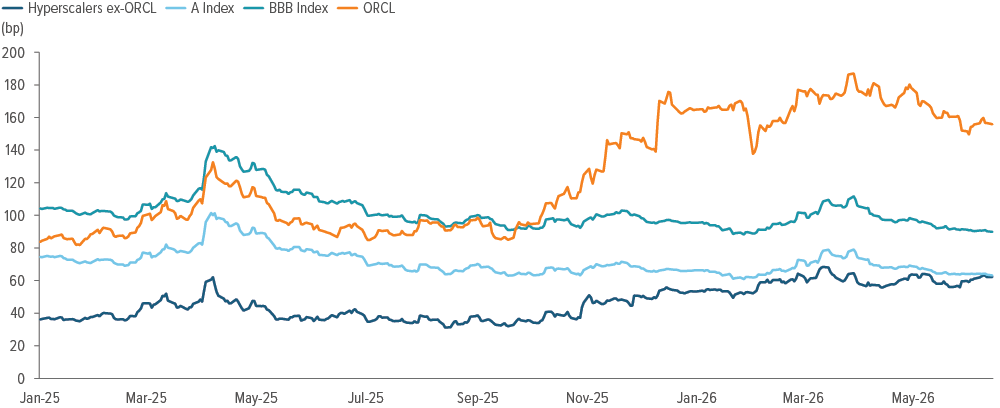

The way data centers are being funded has evolved rapidly over the last 12 months. Beignet Investor (Meta’s Richland Parish data center) was placed privately, but now trades publicly as a 144A at much tighter spread (Exhibit 5).

Since then, the public market has shown that is willing and able to digest data center project bonds with investment-grade guarantors—and has thus become the primary nexus of issuance for them.

As of 06/15/26. Source: Bloomberg; Voya IM. Top bar represents the spread on a hyperscaler’s own US$ bond; second bar is the spread on the data center project bond associated with that hyperscaler.

We view IG hyperscaler and IG data center project bonds as complimentary.

Hyperscaler bonds are higher-rated and have broader businesses and non-AI cash flows that can support the AI capex/growth story, while the data center projects are just that: individual projects with a much more concentrated risk exposure at a BBB rating.

For a primarily IG credit investor, there’s a place for both types of bond in a portfolio for diversification, with the caveat that exposure needs to be managed holistically across hyperscalers and hyperscaler offtakers.

The high yield bond market has also seen $42 billion of data center debt issuance in the past year alone.4 However, we are avoiding medium or long duration below investment grade data center debt in both the private and public markets.

Data center securitizations: Square pegs, round holes

Structural concerns have broadly kept us out of the $21 billion data center CMBS market, despite some attractive spreads on AAA tranches.5 The amount of leverage in CMBS plus extension risk on deals with anticipated repayment dates (ARDs) has not provided the comfort we need to invest.

We note especially that post-ARD coupon step-ups meant to encourage the borrower to refinance do not usually flow through to the CMBS holders, who bear all of the extension risk and none of the reward. We are still fans of traditional CMBS, but the mishmash of structures we’ve seen so far from data center CMBS have not been encouraging (Exhibit 6).

As of 06/18/26. Source: Bloomberg; Voya IM.

Structure is also a problem for us in the $43 billion data center ABS market. In both data center CMBS and ABS markets, it feels like eager issuers are trying to shove square pegs into round holes.

For example, data center ABS tend to be rated on a loan to value (LTV) basis, when LTV is largely irrelevant. The operating expenses of these bonds are too high—and, like their underlying rents, too unpredictable—to be appropriate for an ABS structure.

The same ARD structure that gives us pause in CMBS is also prevalent in data center ABS, raising refinancing risk. On top of that, data center ABS have been around longer so tend to have older collateral more prone to obsolescence risk.

Lastly, data center ABS contain a higher concentration of colocation data centers, which have shorter leases and more merchant risk. That makes them considerably riskier than a hyperscaler lease where the hyperscaler is buying all the compute over a long lease.

Shorter-dated private debt: More diverse options, a little more appetite for risk

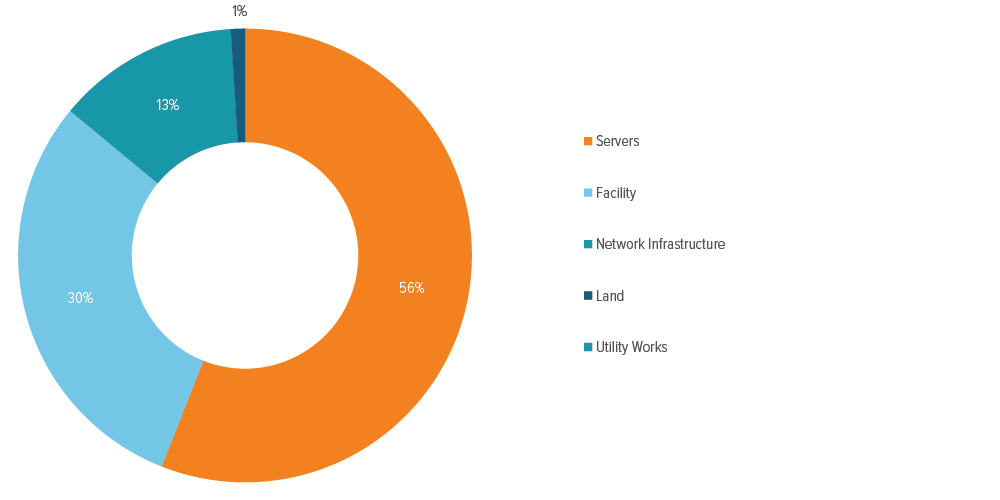

There are interesting shorter-term private placements coming to market related to the AI boom. The obvious one is GPU financing, given that GPUs are over 50% of data center construction cost (Exhibit 7). We have participated in a couple GPU financing deals that were guaranteed by investment-grade sponsors.

As of 06/15/26. Source: Epoch AI.

The guarantee is important—GPUs share the same risks as data centers if there is a setback in the AI growth story. Plus, we haven’t been through a full upgrade cycle for AI data center GPUs yet, so their depreciation schedule remains educated guesswork.

Short-dated private debt is the only place where we’re looking at below investment grade transactions—specifically in construction finance. There have been interesting offerings at attractive spreads for data center, digital infrastructure, and power generation construction finance.

The deals we like are ones with an experienced developer where all major permits are in place, leases or offtake agreements are contracted, and the project is broadly de-risked.

These construction loans tend to be refinanced into lower-spread, longer-term placements as the data center or generation plant is close to becoming operational, providing a natural exit point.

The Voya advantage

One of the biggest risks we see for investors in the AI debt boom is unintentional concentration risk across mandates, with managers each loading up on the “best” AI debt options in their particular asset class.

Compounding this is that there are very few managers like Voya, which has longstanding, in-house expertise across the full spectrum of sectors issuing AI debt: investment grade private placements, ABF, project finance, IG corporate bonds, high yield, and securitized credit.

We are able to look at risk and relative value across fixed income portfolios to pick the right AI debt offerings overall, not just the right ones in each asset class.

We would welcome the opportunity to discuss how our multi-sector fixed income expertise can help you navigate the AI debt boom.

A note about risk: The principal risks are generally those attributable to bond investing. All investments in bonds are subject to market risks as well as issuer, credit, prepayment, extension, and other risks. The value of an investment is not guaranteed and will fluctuate. Market risk is the risk that securities may decline in value due to factors affecting the securities markets or particular industries. Bonds have fixed principal and return if held to maturity but may fluctuate in the interim. Generally, when interest rates rise, bond prices fall. Bonds with longer maturities tend to be more sensitive to changes in interest rates. Issuer risk is the risk that the value of a security may decline for reasons specific to the issuer, such as changes in its financial condition. High yield securities, or “junk bonds,” are rated lower than investment grade bonds because there is a greater possibility that the issuer may be unable to make interest and principal payments on those securities. Foreign investing does pose special risks, including currency fluctuation, economic and political risks not found in investments that are solely domestic. Emerging market securities may be especially volatile. Investments in mortgage-related securities involve exposure to prepayment and extension risks greater than investments in other fixed income securities. The strategy may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and could have a potentially large impact on performance. Investments in commercial mortgages involve significant risks, which include certain consequences that may result from, among other factors, borrower defaults, fluctuations in interest rates, declines in real estate values, declines in local rental or occupancy rates, changing conditions in the mortgage market, and other exogenous economic variables. All security transactions involve substantial risk of loss. The strategy will invest in illiquid securities and derivatives and may employ a variety of investment techniques, such as using leverage and concentrating primarily in commercial mortgage sectors, each of which involves special investment and risk considerations. Other risks include, but are not limited to: credit risks; credit default swaps; currency; interest in loans; liquidity; other investment companies’ risks; price volatility risks; inability to sell securities risks; U.S. government securities and obligations; sovereign debt; and securities lending risks.