Private assets have an important role in enhancing long‑term defined contribution retirement outcomes.

The retirement industry’s evolution

Saving for retirement is American families’ number one reason for saving, and 54% of families possess some type of retirement account—whether it be an IRA, target date fund, or managed account.1 The 66 million American workers who are participants in retirement savings plans are now more than ever looking to sponsors for confidence in their financial futures.2

The retirement industry has continuously evolved in response to participant needs and legislation. Target date funds gained wide-scale adoption in 2006 because of the Pension Protection Act, making them the qualified default investment alternative for retirement savings plans. In 2023, Secure 2.0 auto-enrollment and auto-escalation of participant savings changed from suggested to required for almost all new plan participants and new corporate and nonprofit savings plans.

Over the last two decades, target date funds have transitioned from the rudimentary investment options of only U.S. equities and fixed income to globally diversified portfolios.

We see the next step in the retirement industry’s evolution as the introduction of alternative investments, such as private equity, real estate, and private fixed income, into target date funds. This mirrors the risk and return opportunity set that has long been available to large institutional defined benefit pension programs.

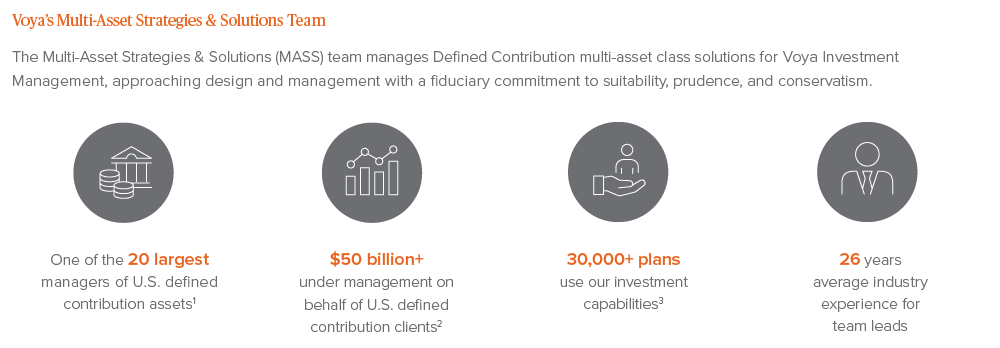

As fiduciaries with over 20 years of experience managing target date funds, managed accounts, and retirement assets, we believe that adding alternative investments can play an important role in a diversified retirement portfolio.

Our research shows that alternative investments can create better retirement outcomes and potentially boost participants’ defined contribution final account balance by more than 8% over a 40-year working career.

This means participants can feel more optimistic about their financial future in retirement, with the potential of extra income to ease the strain of everything from unexpected repair bills to surprise visits from the grandkids.

How sponsors can integrate private assets into defined contribution plans

As defined contribution plans continue to evolve, plan sponsors and participants alike are asking thoughtful and important questions about how to use private assets to enhance diversification and improve long-term investment outcomes. This briefing offers a practical example of how private assets can be incorporated into a target date solution, highlighting ways to enhance participant outcomes through strategic portfolio design.

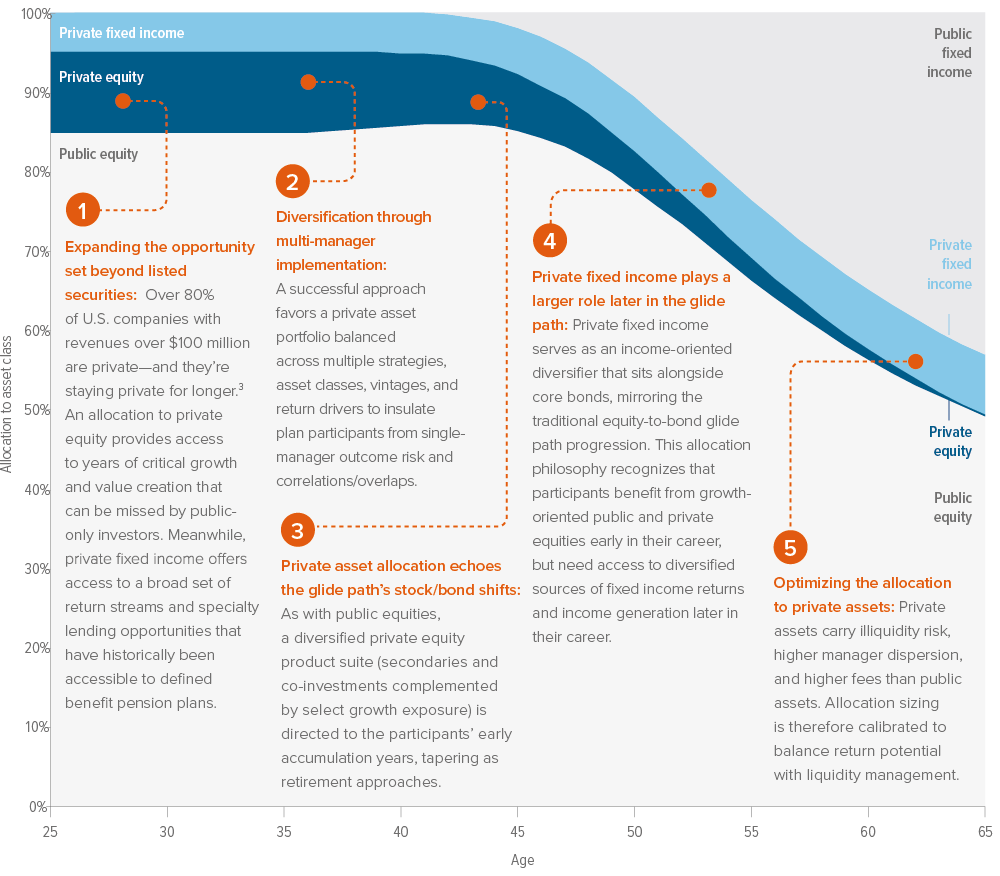

Our illustrative glide path incorporates private asset allocations that peak at approximately 15% of the portfolio during early career stages and taper to around 7.5% at retirement. In our view, this properly balances not only plan participants’ need for returns but also their liquidity needs as retirement nears.

In our example, the inclusion of private assets over a 40-year working career results in a potential boost of 8.2% in final account balances versus a public asset-only portfolio. This could translate into over $800 a month in additional post-retirement income for participants.

In choosing how to allocate to private assets, we favor a diversified, multi-manager implementation, echoing best practices in public investments asset allocation. For private equity, including secondaries and co-investments can improve diversification across managers, sectors, and vintages. For private fixed income, diversifying across corporate credit, specialty finance, and mortgage-linked strategies with differing structural sensitivities can help balance exposure across market regimes.

Voya’s significant presence in the investment grade private placement market is an important differentiator, allowing integration of higher-quality private fixed income assets alongside the more typical speculative-grade private credit offered by the majority of direct lending funds.

Adding alternative investments to a defined contribution plan has the potential to boost participants’ defined contribution final account balance by 8.2% over a 40-year working career. |

Source: Voya. Outcomes based on stochastic analysis of 50,000 economic scenarios. This example is for a sample defined contribution target date portfolio with above-average participant earnings and a cash balance plan. Assumptions: Voya 2026 equilibrium capital market expectations. Private market allocations over the life of the plan are illustrated in the glide path, overleaf. Private equity modeled as Buyouts. Private Fixed Income modeled as a blend of direct lending and investment grade private credit. Starting age of 25 and retirement age of 65. Total annual contributions are 16%. Best-case is represented by the 95th percentile balance and worst case by the 5th percentile balance at retirement age. Monthly post-retirement income is the maximum withdrawal at retirement age that results in a non-zero balance in 90% of the longevity and capital market scenarios. The projections regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results.

Illustrative target date glide path incorporating private assets

Using extensive experience and proprietary data, Voya’s Multi-Asset Strategies & Solutions team calculated a target date glide path for a hypothetical plan sponsor, modeling potential private market returns alongside typical public market allocations. This glide path depicts the allocations leading to the participant outcomes.

Best practices for implementing private assets

Private market investments are increasingly part of a broader conversation among defined contribution participants. Retirement surveys now regularly point to high levels of interest among participants in private asset offerings— but often low levels of knowledge.4 This points to a critical factor: having the right guardrails in place.

62% of participants in Voya workplace retirement savings plans say they are interested in their plan providing access to private assets.5 |

When it comes to introducing complex investments like private credit, private equity, and other alternatives into defined contribution plans, we believe that professionally managed investment products, such as advisor-managed accounts, collective investment trusts, or registered fund structures, represent appropriate starting points.

These solutions allow for oversight at the participant level, incorporating factors such as age, retirement horizon, savings behavior, and risk tolerance into ongoing portfolio management.

We believe capturing the return streams of private assets is best realized through thoughtful integration that is aligned with the distinct characteristics of public and private markets.

Cost considerations are important when incorporating alternative investments into target date funds, especially given the long-term nature of the investments and participants’ fee sensitivity. Alternatives often carry higher management fees and underlying vehicle costs, making it essential to assess the whether the potential diversification, return, and risk mitigation benefits meaningfully offset the incremental fees.

Thoughtful structuring, scale, and manager selection can help control total plan-level expenses while maintaining alignment with fiduciary expectations and participant outcomes.

Liquidity is another significant factor to weigh when adding alternative investments to a defined contribution target date fund, as participants expect daily liquidity and the ability to rebalance efficiently. Many alternative strategies involve longer lockups or less frequent valuation cycles, requiring careful structuring to preserve participant-level liquidity.

Our discipline includes maintaining a liquidity sleeve inside our multi-manager alternative investment strategies to ensure the target date fund can meet cash flows, rebalancing needs, and participant transactions without introducing unintended risks.

Grounded in our research, the glide path approach helps investors thoughtfully incorporate private assets. |

Expanding investment choices in retirement plans should never be an end in and of itself. The goal remains to help participants achieve better long-term outcomes, and that requires governance, transparency, education, and thoughtful implementation.

Next steps

As interest in private market investments continues to emerge, professionally managed vehicles offer a prudent path forward. They reflect a belief we’ve long held at Voya: that access without guidance is not empowerment.

Professional oversight, paired with strong fiduciary frameworks and robust plan level resources, is what allows innovation to coexist with responsibility.

We welcome continued dialogue on how we can improve plan participants’ financial futures together.

1 As of June 2025, P&I ranked Voya 20 out of 155 firms surveyed based on total US institutional DC AUM. Participation in the P&I ranking is voluntary and open to firms that manage assets for U.S. institutional tax-exempt clients. Managers self-report their data via a survey. P&I sends the survey to previously identified managers and to any new managers asking to participate in the survey/ranking. No fee was paid for consideration.

2 AUM as of 12/31/25; the DC Assets excludes approximately $33 billion in assets under administration. 3 As of 12/31/25.

A note about risk: Target date funds are subject to the risks of the underlying funds and asset classes in which they invest. The target date is the approximate date when investors plan to retire. The principal value of the fund(s) is not guaranteed at any time, including at the target date. Asset allocation does not ensure profit or protection against a loss. When used in a retirement plan, private market investments may introduce additional risks, including limited liquidity and transfer restrictions, valuation uncertainty, higher fees and complexity, and operational/administrative considerations; they may not be suitable for all participants and could adversely affect participant outcomes.