A Guide to Investment Grade Private Credit

Managing Director, Head of Private Credit

Senior Vice President, Head of Portfolio Strategy

Senior Vice President, Portfolio Manager

Senior Vice President, Portfolio Manager

With attractive yields, robust covenant protection, and ample liquidity, investment grade private credit is a growing favorite of both investors and borrowers. Here’s what you need to know.

Executive summary

- The $2+ trillion investment grade (IG) private credit market is used by nearly all U.S. life insurers and about half of U.S. pension funds as a complement to IG bonds for diversification and income enhancement.

- For investors, the asset class has historically offered attractive return premiums to equivalent corporate bonds, as well as enhanced loss mitigation and ample liquidity.

- For issuers, the asset class provides meaningful advantages such as customization, more certainty of execution, privacy, and the ability to handle complex collateral.

- Expanding issuer and investor bases are leading to increasing deal volumes, larger transaction sizes, and wider opportunities across the three types of IG private credit placements: corporate, infrastructure, and asset-based finance (ABF).

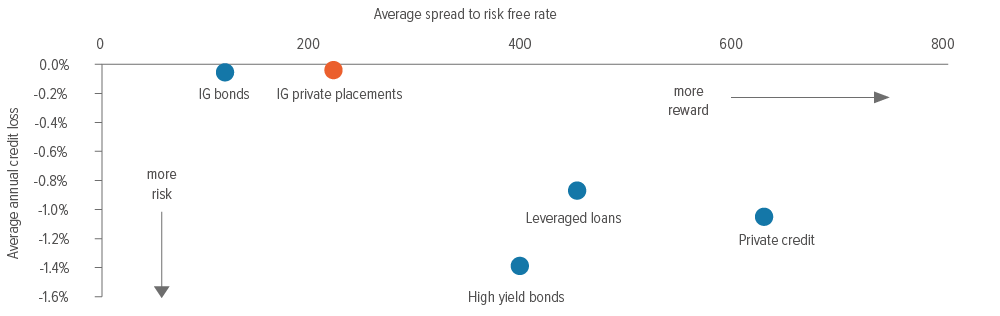

As of 03/31/26. Source: Voya IM, Standard & Poors, Morningstar, Cliffwater, Pitchbook, BofA. Average annual credit loss and average spread over risk free are measured over the 10-year period 01/01/16-12/31/25; IG corporate bond credit loss derived from default rates with an assumed 45% average recovery rate.

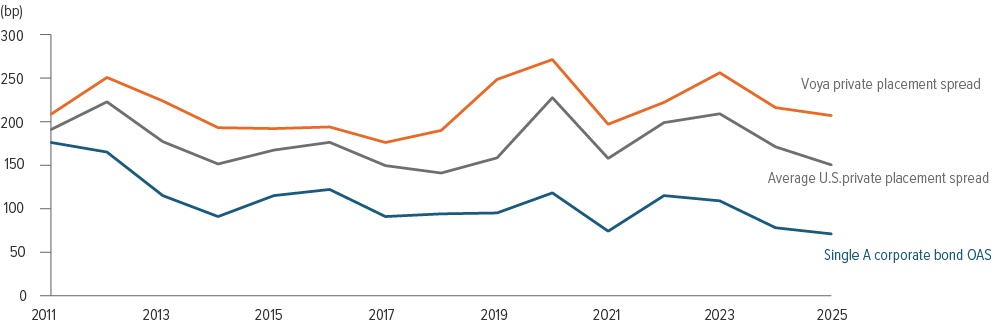

As of 03/31/26. Source: Voya IM, BofA, FRED. Private credit spreads based on a BBB+/A- portfolio, 66% NAIC 2 assets and 33% NAIC 1 assets.

What is investment grade private credit?

When the media talks about “private credit,” it usually means speculative-grade direct lending to middle market companies, an asset class whose growth was spurred by post global financial crisis limitations on bank leveraged lending.

However, there is also a separate market for non-bank lending that grew up decades earlier in response to life insurers’ need for high-quality, long-term investments to match their liabilities: the $2+ trillion investment grade private credit market. Historically, this was referred to as the U.S. private placement market.

Over the past decade, the investor base for investment grade private credit has diversified well beyond life insurers to pension funds, endowments, large family offices, P&C insurers, and more. Life insurers remain the largest investors, though, with some $1.5 trillion of issuance sitting on their balance sheets.1

Functionally, investment grade private placements are a hybrid of a public bond and a traditional bank loan. They share characteristics with public bonds, including being rated by a nationally recognized securities rating organization and/or the National Association of Insurance Commissioners, and having fixed maturities of 3-30 years. Similarities with bank loans include greater upfront due diligence, priority debt and financial covenant protection, and a more engaged relationship with borrowers.

Where investment grade private placements differ from both bonds and bank loans is the ability to offer custom tenors and features (such as delayed draws, amortization features, foreign currencies, and non-index deal sizes) as well as a willingness to take on complex structures and collateral that require higher levels of due diligence.

These debt offerings are private because the notes are sold only to qualified institutional buyers (QIBs2) and, as such, do not have to be registered with the U.S. Securities and Exchange Commission (SEC), enabling issuers to keep their financial details out of the public eye. For purposes of this paper, the terms “investment grade private credit” and “private placements” refer to Regulation D securities3 and do not include securities issued under Rule 144A.4

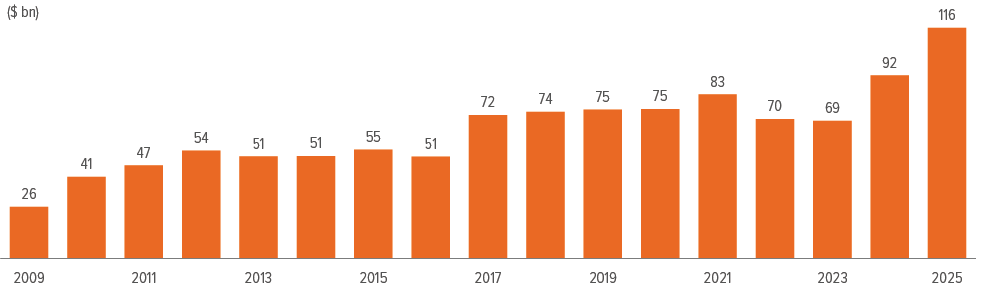

As of 05/15/26. Source: Voya IM estimates, Reg D filings, StoneCastle, BofA. Spreads calculated from the Voya Private Credit Strategy and General Account total production, 01/01/03-03/31/26.

While private placements are available in all rating categories, the majority of issuance is done by borrowers with credit quality between A- and BBB-.5 The size of the borrowers varies, with revenue of issuing companies generally ranging from $250 million to over $200 billion.

The majority of deals (85%) are marketed by intermediaries to either the entire market of participating QIBs or a subset of the market. Only 10-15% of deal volume in the investment grade private credit market is direct, (unagented), as few investors have the scale to commit to direct transactions when the average deal size is in the hundreds of millions.6

An expanding opportunity

The investment grade private credit market is currently in a dynamic growth phase, thanks to an influx of new originators, a broadening investor base, proven and improving liquidity characteristics, and strong demand from borrowers. These borrowers are not just private companies (over 80% of U.S. companies with revenues greater than $100 million are private7), but also select foreign borrowers and large public companies.

It’s not just volumes that are growing. The investment grade private credit market has also seen noticeable increases in average transaction size over the past several years, along with greater diversification of collateral and deal structure.

Prior to 2000, most investment grade private placements were small transactions of less than $100 million. Since 2000, deal sizes have almost quadrupled, with most now averaging about $375 million—and $1 billion+ transactions getting done with reasonable regularity.

Why borrowers choose the investment grade private credit market

|

As of 03/31/26. Source: Bank of America U.S. Private Placement Market Snapshot.

A note about risk Private placements are generally investment grade assets, and like all investments, there are risks associated with investing in a portfolio of private placements. Risks described below are not all-inclusive, and before making an investment in a portfolio of private placements, investors should carefully consider such an investment. The primary risk to an investment in private placements is credit risk. Credit risk is the risk of non-payment of scheduled interest or principal payments on a debt instrument. In the event a borrower fails to pay scheduled interest or principal payments on its debt, a portfolio of private placements would experience a reduction in its income and a decline in market value. Private placements generally involve less risk than unsecured or subordinated debt and equity instruments of the same issuer because the payment of principal and interest on private placements is a contractual obligation of the issuer that, in most instances, takes precedence over the payment of dividends, or the return of capital to the borrower’s shareholders and payments to public bond holders. In the event of the bankruptcy of a borrower, a creditor could experience delays in receiving regular payments of interest and principal and may not receive the full repayment of its principal. Portfolios of private placements are also subject to interest rate risk. One risk related to interest rates is the potential for changes in the interest rate spreads for private placements in general. To the extent that changes in market rates of interest are reflected not in a change to the base rate, the U.S. Treasury, but in a change in the spread over the base rate which is payable on loans of the type and quality in which a portfolio invests, a portfolio of private placements could also be adversely affected. This is because the value of a debt is partially a function of whether it is paying what the market perceives to be a market rate of interest, given its individual credit profile and other characteristics. However, unlike changes in market rates of interest for which there is only a temporary lag before a portfolio reflects those changes, changes in a placement’s value based on changes in the market spreads on loans may be of longer duration. If spreads rise as described above, for example, in response to deteriorating overall economic conditions and/or excess supply of new loans, the principal value of private placements may decrease in response. On the other hand, if market spreads fall, the value of private placements may increase in response, but borrowers also may renegotiate lower interest rates on their debts or pay off their debts by refinancing at such lower rates. In that case, the borrowers would be required to pay a makewhole amount, which would mitigate the risk. Private placements trade in a private, unregulated market directly between loan market participants; although most transactions are facilitated by broker-dealers affiliated with large commercial and investment banks. As a result, purchases and sales of private placements typically take longer to settle than similar purchases of bonds and equity securities. In addition, because private placement transactions are directly between investors, there can be greater counterparty risk. Moreover, despite the increase in the size and liquidity of the private placement market, the market is still relatively illiquid, particularly when compared to the markets for bonds and equities. As a result, portfolios invested in private placements may experience difficulties and delays in purchasing or selling private placements, with resulting adverse impacts upon the prices obtained. During periods of severe market dislocation, such as occurred at the end of 2007 and during 2008, the market can experience severe illiquidity and significantly depressed prices. Finally, many borrowers are private companies and/ or companies that have not issued other debt that is rated by rating agencies such as Moody’s Investors Service, Standard & Poor’s, or Fitch Ratings. As a result, investment decisions related to private placements may be based largely on the credit analysis performed by the adviser to the fund or portfolio making the investments, and not on rating agency evaluation. This analysis may be difficult to perform. Information about a private placement and the related borrower generally is not in the public domain, since private companies and companies that have not issued public debt or securities are not subject to reporting requirements under federal securities laws. However, borrowers are required to regularly provide financial information to lenders, typically in much greater detail than is available in the public markets. Furthermore, information about borrowers may be available from other private placement participants or agents who originate or administer private placements. |