Unconstrained Fixed Income: Perspectives on Duration

Head of Multi-Sector Fixed Income

Key Takeaways

Traditional fixed income often leaves investors unprotected from prevailing market risks, due in part to a habit of focusing on spread first and duration later.

Duration should be an integral part of portfolio construction—and maintaining duration exposure can improve diversification and help mitigate the impact on returns of periods of credit stress.

The Voya Unconstrained Fixed Income Strategy uses a disciplined duration framework with a central tendency of two years, a duration historically associated with the lowest absolute return volatility, to support the strategy’s objective of delivering consistent risk-adjusted returns across market environments.

Voya’s Unconstrained Fixed Income Strategy seeks to provide consistent risk-adjusted returns over a full market cycle by using duration to help mitigate spread volatility.

Establishing risk parameters

For many investors, the primary function of fixed income is to protect wealth and achieve moderate returns over the long term while avoiding downside risk. When investors instead focus on maximizing short-term returns, they usually do so by reaching for risk, which can prove problematic in today’s turbulent credit markets. A target is only worthwhile if you can hit it consistently.

We believe that establishing prudent risk tolerances before setting return expectations is likely to lead to more consistent and reliable investment returns. This is the guiding principle behind the Voya Unconstrained Fixed Income Strategy:

First, identify a rational level of risk tolerance for the client and adjust return expectations in each market for that stated risk tolerance. Then, using the risk tolerance and return expectations, craft an optimized portfolio of fixed income securities that seeks to produce consistent returns in any market environment. |

How is the risk objective determined?

The central objective of the Voya Unconstrained Fixed Income Strategy is not simply to protect investors from rising rates, but also to produce positive performance regardless of the market environment.

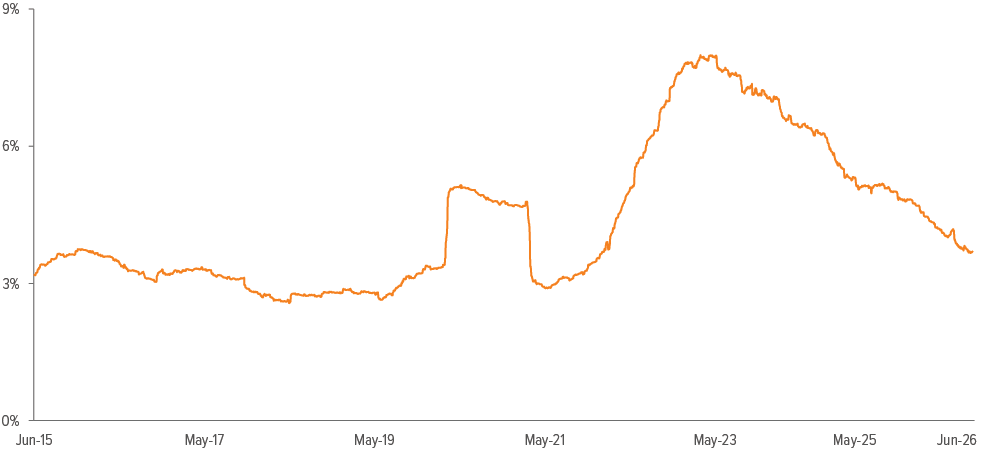

By taking a longer-term perspective, the strategy is able to establish a clear risk tolerance before considering specific, quantifiable return objectives. Accordingly, for the unconstrained strategy, we expect volatility to be in line with traditional fixed income, which is represented by the long-term volatility range of the Bloomberg Barclays U.S. Aggregate Bond Index Exhibit 1.

As of 06/30/26. Source: Bloomberg.

Even with the added flexibility afforded by such an approach, we believe an unconstrained strategy still should behave like a fixed income investment and should exhibit a risk profile consistent with traditional fixed income assets. Using risk tolerance as our primary guide, we focus on producing more consistent returns while attempting to minimize downside risk.

We intend for the unconstrained strategy to provide protection from volatile equity markets in a fashion similar to traditional fixed income strategies, as well as to produce consistent returns over a full market cycle. In addition, the flexibility of the strategy and its tightly managed risk profile are intended to provide investors with a more stable return experience than traditional fixed income products, i.e., enhanced downside risk mitigation and limited volatility.

How is duration optimized?

With the rationale for the risk objective now established, we can move to the strategy’s central tendency for duration, which is set at two years. This is based on long-term data that demonstrate clear, recognized diversification benefits associated with mixing duration risk and credit risk.

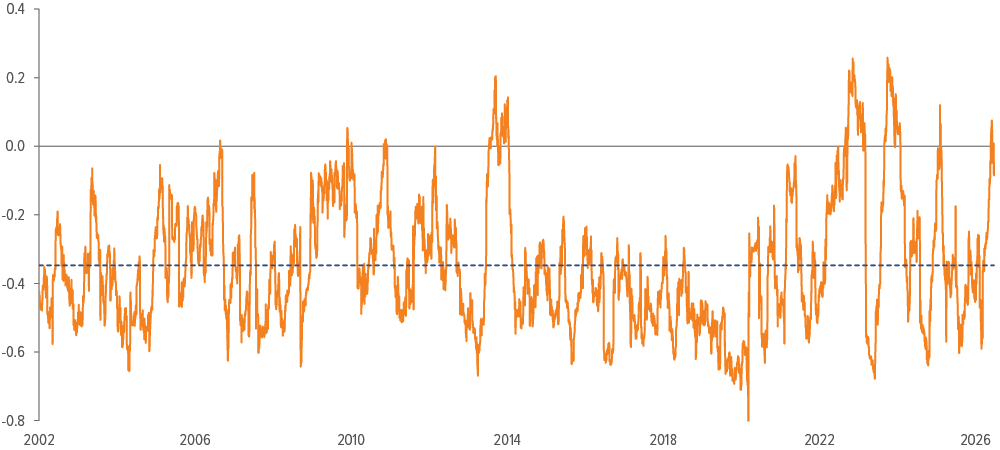

Exhibit 2 shows a generally negative correlation over the last 25 years between Treasury securities (a gauge of duration risk) and corporate bond spreads (a gauge of credit risk).

As of 06/30/26. Source: Bloomberg.

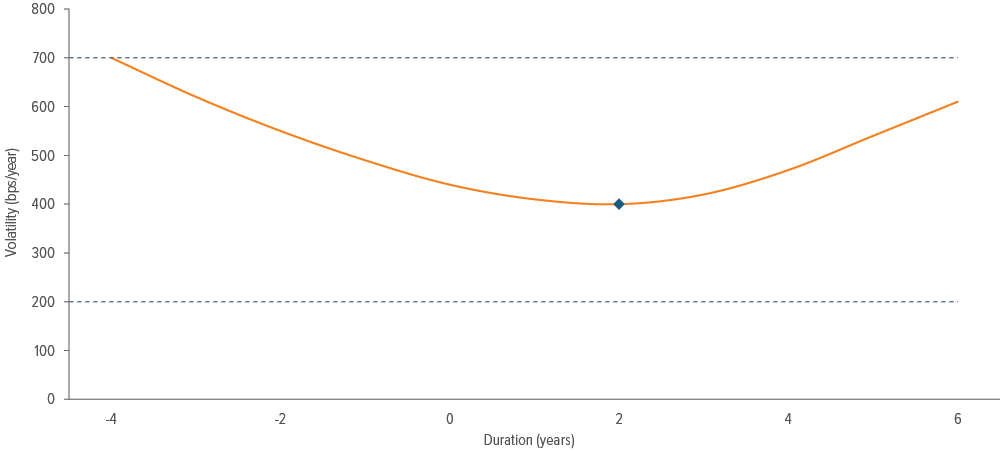

Assuming the correlation of Exhibit 2 holds true in the future, you can then plot the projected volatility of a hypothetical portfolio as duration changes. The starred point on the orange “historical volatility” line of Exhibit 3 shows that a portfolio of investment-grade and below-investment-grade fixed income securities (“diversified portfolio”) exhibits its minimum volatility at a duration of about two years, which is why this point represents the strategy’s duration central tendency. Keeping credit risk constant, overall portfolio risk increases as duration rises or falls from this point. We believe two years represents an optimal balance of risk and reward over the long term.

While a duration of two years is the long-term central tendency, given the unconstrained nature of the strategy, we can still adjust duration above and below this point in the short term. However, we limit the portfolio’s range of duration to -2 to 6 years, which we have determined to be optimal for staying within the stated risk objective of 200–700 bp as outlined above.

We believe this range maximizes flexibility while ensuring that the strategy remains within its risk budget even as market conditions change. A wider duration range brings significant potential.to exceed the risk budget and/or limits the strategy’s flexibility.

Source: Voya Investment Management. Shown for illustrative purposes only.

This can be illustrated best by looking at a point outside the strategy’s duration range. For example, the -4 year duration point has an absolute volatility just short of 700 bp. While this falls within the permitted volatility range for the strategy, it constrains the portfolio in two significant ways:

- Provides no room to further increase credit risk: The strategy’s unconstrained mandate is designed to allow for tactical increases or decreases of credit risk from the diversified portfolio. Because credit risk and positive duration risk are negatively correlated, it follows that credit risk and negative duration risk are positively correlated. Therefore, increasing credit risk beyond the diversified portfolio would increase overall risk and likely cause the portfolio’s absolute volatility to exceed the 700 bp maximum.

- Assumes long-term correlations always hold: While Exhibit 2 shows that duration and credit risk have a consistent, long-term negative correlation, it also makes clear that this relationship is volatile. At times this correlation has moved close to zero and occasionally has turned positive. It cannot be assumed that the potential diversification benefits of this correlation will always hold; at certain times those benefits may erode or reverse.

The orange line of Exhibit 3 shows what happens to portfolio risk in a worst-case scenario—when the correlation benefits in the diversified portfolio disappear. It is important to appreciate and utilize the long-term diversification benefits that correlations provide, but it also is important to recognize that these benefits are not constant or permanent. Limiting duration to the range shown in Exhibit 2 allows for appropriate flexibility while providing a cushion to help the portfolio comply with its absolute risk objective, should the credit/ duration correlation benefits diminish.

These two points highlight the dangers of exceedingly wide duration bands. The Voya Unconstrained Fixed Income Strategy’s duration range is designed to stay within well-defined risk and return parameters. This design provides the necessary flexibility to tactically adjust risk exposures in the portfolio as market conditions change.

We believe that centering the duration range around two years provides for optimal diversification of portfolio risks without introducing the potential for greater volatility that could result from overly wide duration bands.

Clearly defined risk tolerances, not specific return targets, are most important when approaching today’s challenging fixed income markets. The Voya Unconstrained Fixed Income Strategy’s flexible investment mandate, guided by carefully designed risk parameters, takes these challenges into account as it seeks to deliver long-term value to investors.

A note about risk

Unconstrained fixed income: The principal risks are generally those attributable to bond investing. Holdings are subject to market, issuer, credit, prepayment, extension, and other risks, and their values may fluctuate. Market risk is the risk that securities may decline in value due to factors affecting the securities markets or particular industries. Issuer risk is the risk that the value of a security may decline for reasons specific to the issuer, such as changes in its financial condition. The strategy may invest in mortgage-related securities, which can be paid off early if the borrowers on the underlying mortgages pay off their mortgages sooner than scheduled. If interest rates are falling, the strategy will be forced to reinvest this money at lower yields. Conversely, if interest rates are rising, the expected principal payments will slow, thereby locking in the coupon rate at below market levels and extending the security’s life and duration while reducing its market value. High yield bonds carry particular market risks and may experience greater volatility in market value than investment grade bonds. Foreign investments could be riskier than U.S. investments because of exchange rate, political, economics, liquidity, and regulatory risks. Additionally, investments in emerging market countries are riskier than other foreign investments because the political and economic systems in emerging market countries are less stable.