Get the latest insights from our securitized credit desk.

After a Q1 hiatus, securitized credit market talking points are back! We are looking to streamline the macro (easier said than done), focus-in on the guts of the market and make it more efficient with your mind share.

On that front…tricky macro backdrop indeed, but reassuring stability in securitized that we will bring to life for you.

As always, thrilled to receive any feedback or follow-up…

- While we’d like to be “pure” with securitized color, it is difficult when our market dynamics have been over-shadowed by the macro backdrop to this degree.

- After a great start to the year in January, AI displacement fears started rolling through different industries believed to be exposed during the month of February.

- This has been with us since then, impacting CLO markets most directly given exposure to potentially vulnerable companies borrowing in the leveraged loan market.

- Right or wrong, we have conflated AI displacement risk with the disruption in private credit markets, which has been plagued by redemptions from a comprehensive array for funds and BDCs.

- While public securitized markets aren’t directly impacted, most of the operators are active participants in securitized markets, whether as investors or issuers or both, so we are watching closely for any follow-on distortions that may emerge. To be clear, we haven’t seen evidence of any fallout.

- In more recent weeks, the conflict in Iran have driven day-to-day swings in risk sentiment, with energy prices the key cudgel in markets.

- Thankfully, direct feedback loops into securitized are limited from this geopolitical dimension, so impact has manifested mainly as day-to-day changes in sentiment and market tone.

- After a great start to the year in January, AI displacement fears started rolling through different industries believed to be exposed during the month of February.

- Throughout, US economic growth drivers have been reasonably stable and supportive of risk-taking.

- Fed policy has been an exception given budding inflation concerns, which has fed through into rate volatility.

- This had direct impact on total returns and bond yields, with agency MBS sectors the most impacted given more measurable negative convexity attributes.

- This has cut both ways, with the more recent drop in rate vol and accompanying rally in rates allowing retracement and outperformance in agency sectors.

- Fed policy has been an exception given budding inflation concerns, which has fed through into rate volatility.

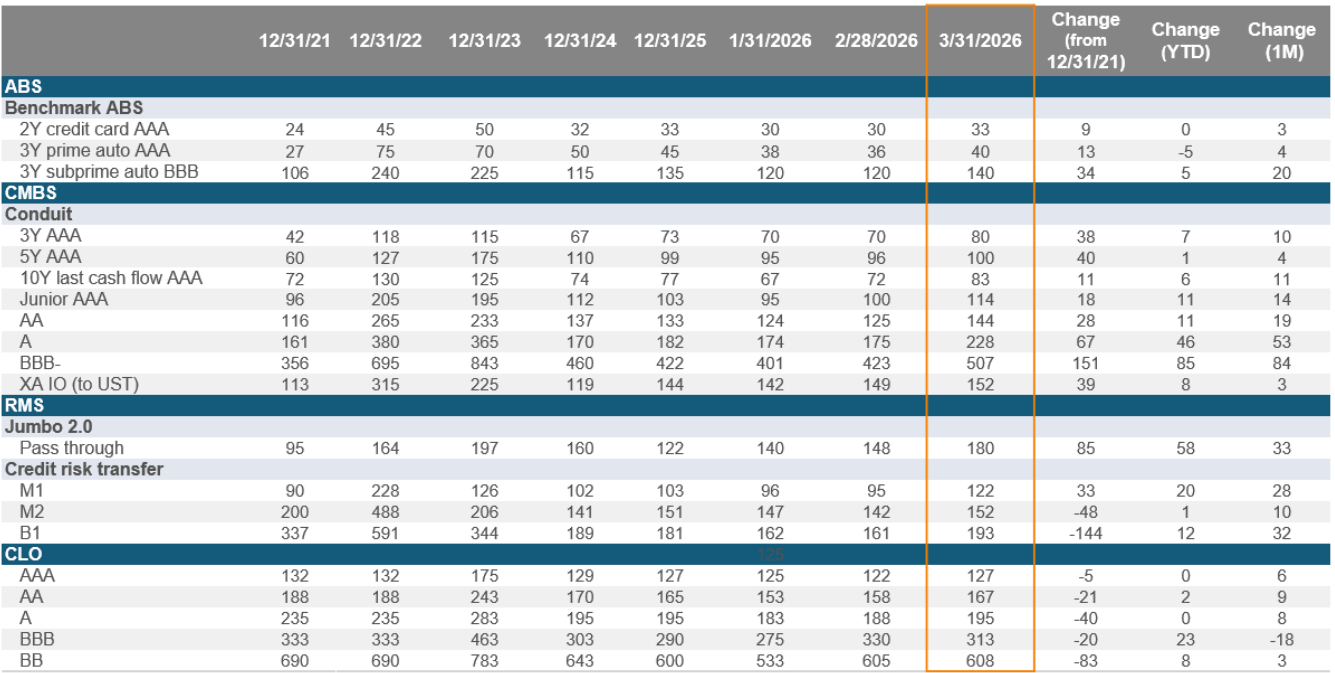

Source: Voya Investment Management, JP Morgan, Bank of America, Bloomberg. As of 3/31/2026.

- We characterize the move in securitized as moderate. And being the market day-to-day, it transpired that way with vol a fraction of what the broader markets endured. New issue and secondary markets remained fully functioning throughout, with only narrow pockets of measurable spread volatility (BB CLOs, current coupon MBS). This mostly reflects, in our estimation, the less direct influence of the macro risks in play.

- But, we concede that things did ultimately push wider, in sympathy with broader markets as weaker sentiment took hold and liquidity became more expensive, particularly as we approached quarter end.

- CLOs underperformed: the closest sector to AI disruption risk and private credit fears. Credit curves steepened and the complex decompressed, with manager tiering again apparent and the basis between BSL and Private Credit CLOs more measurable.

- N.A. RMBS wider but uncorrelated and refreshingly actionable: heavy issuance cost it some spread widening (see below gross issuance exhibit), with net new issuance (gross issuance less paydowns) by far the biggest across securitized sectors at $34B (source: JPM). Risks remain well insulated and the day-to-day vol was perhaps the least correlated with broader markets of any of the securitized sectors.

- CMBS sneaky outperforming with new issue-centric weakness: the pace of issuance was judicious, but that which came suffered and accounts for the widening displayed above. More seasoned parts of the universe endured less measurable spread widening, reflecting the market’s unwillingness to part with bonds that would like prove harder to replace.

- We are buyers of this move, upgrading various new issue CMBS sub-sectors (see updated LLL exhibit for April).

- ABS outperformed: in the back end of March, when liquidity was most expensive, it displayed the most issuer discipline, clocking the lightest amount of gross issuance across sectors (<$5B). Regular way consumer risk trading well throughout, even subprime flavors. Some more measurable widening noted in digital infrastructure sub-sectors (data center, fiber ABS).

Securitized Credit Issuance

In addition to what was highlighted above in the Q1 experience, I’d only add that the start to Q2 has been measured. Overall pipelines have been slower to be deployed, but they remain visible and we expect to get very busy in coming weeks. In particular, we expect non-agency RMBS and ABS to risk upsetting the supply-demand balance that has been quite friendly MTD in April. CLO and CMBS we expect to get heavier but be on the lighter side, at least relative to 2025 volumes.

Outlook

- The set-up in securitized credit markets is favorable for risk takers, strategically but especially tactically. The run-up in equities and corps MTD is feeding through to securitized, with the front end of the new issue pipeline likely to catalyze some more measurable spread tightening.

- As we proceed through the pipeline, there is risk of some sloppiness emerging, particularly if timed with any refreshed escalations out of the Middle East. But, we advocate being a buyer of this, essentially liquidity premiums for nimble investors.

- Throughout these next couple of months, we like seasonals to support our always developing fundamentals, with consumer ABS remits and housing market activity expected to show results that support risk taking and sponsorship in our markets.

We hope everyone is enjoying their spring and managing through these markets with success.

Voya Securitized Team