Beyond CCCs: A More Efficient Path to High Yield Returns

Senior Managing Director, Chief Investment Officer, Income & Growth

Managing Director, Lead Portfolio Manager - Income & Growth

Senior Vice President, Lead Portfolio Manager - Income & Growth

Key Takeaways

Convertible structures combine equity participation with bond-like downside support, which helps explain their historical outperformance versus CCC rated bonds.

Lower correlation to higher-quality high yield can diversify return sources beyond traditional credit beta and coupon income.

Replacing CCC exposure with convertibles may improve portfolio efficiency, preserving upside participation while reducing downside capture.

Substituting convertible securities for CCC rated bonds in high yield mandates may improve return potential while reducing reliance on distressed credit risk.

The challenge with CCC exposure

Incremental yield comes with disproportionate credit risk: Within high yield allocations, CCC rated bonds have historically offered only modest incremental return relative to higher-quality high yield, and they introduce substantially greater volatility, default sensitivity, and liquidity risk. The modest return differential is primarily a function of higher coupon income (required to compensate investors for increased risk) minus credit losses from defaults and restructurings. Their increased volatility is primarily the result of higher default risk coupled with reduced liquidity/ownership.

Why convertibles offer a different return profile

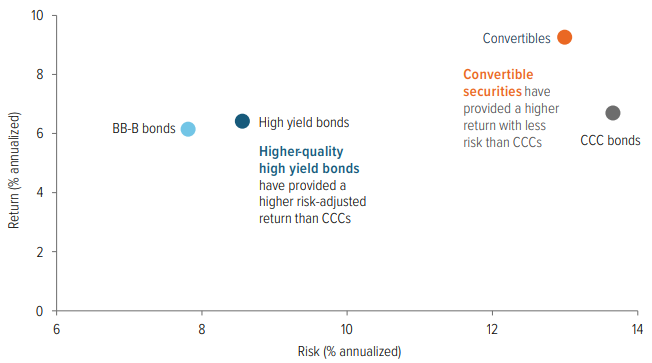

Equity optionality with bond-like downside support: Convertible securities offer a significantly higher return and are less volatile than CCC rated bonds (Exhibit 1). Unlike traditional fixed income, convertibles have characteristics of both equities and bonds that result in an asymmetric return profile. The embedded equity optionality creates participation in issuer upside, while the bond component can help moderate downside relative to lower-quality credit exposure.

Data 01/01/97 to 05/31/26. Source: FactSet, ICE Data Services, Voya IM. Convertibles: ICE BofA U.S. Convertibles Index. high yield/ BB-B/CCC: ICE BofA U.S. High Yield Index and corresponding subindexes. See endnotes for index defintiions.

Diversification beyond traditional credit beta

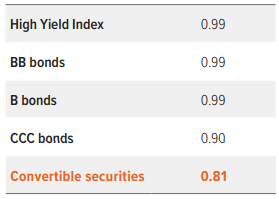

Lower correlation to higher-quality high yield: Beyond return and volatility dynamics, convertibles offer diversification benefits within credit-oriented portfolios. As shown, the ICE BofA U.S. Convertible Index has exhibited a lower correlation to higher-quality high yield bonds (represented by the ICE BofA U.S High Yield (BB-B) Index), than the lowestquality segment (CCC rated bonds). This relationship reflects differentiated return drivers. While high yield bond performance is largely tied to coupon income, convertible security performance is primarily influenced by the movement of the underlying equity, resulting in more varied sources of return.

This combination can enhance portfolio efficiency by reducing reliance on traditional credit beta. In periods when credit spreads, liquidity, and default risk dominate high yield returns, convertibles may serve as a complementary exposure, potentially improving overall portfolio performance across economic cycles.

Data 06/01/06 to 05/31/26. Source: FactSet, ICE Data Services, Voya IM. High yield/BB/B/CCC bonds: ICE BofA U.S. High Yield Index and corresponding subindexes. Convertible securities: ICE BofA U.S. Convertible Index. See endnotes for index definitions.

Portfolio efficiency improves when CCCs are replaced

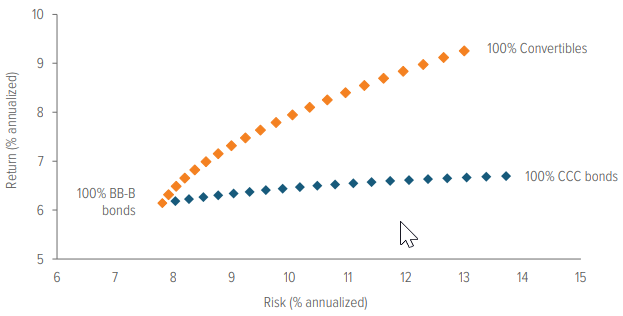

A more efficient risk/return mix: When viewed through a portfolio construction lens, substituting CCC exposure with convertibles has historically improved the efficiency of a high yield allocation. As illustrated, increasing exposure to convertibles shifts the efficient frontier upward and to the left, delivering stronger performance for a given level of risk relative to portfolios with concentrations in lower-quality high yield. By reducing reliance on binary credit outcomes and introducing positive convexity-based return characteristics, convertibles can help improve returns and reduce volatility over time.

Data 01/01/97 to 05/31/26. Source: FactSet, ICE Data Services, Voya IM. Convertibles: ICE BofA U.S. Convertibles Index. BB-B/CCC bonds: ICE BofA U.S. bonds (BB-B) Index and CCC & Lower Index. See endnotes for index defintiions.

Similar upside, less downside

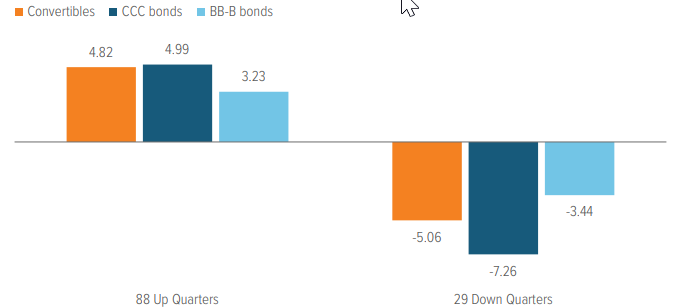

Market participation with better asymmetry: Examination of upside and downside capture rates reveals diversification benefits from a different perspective. Exhibit 4 anchors market participation to quarterly returns of the ICE BofA U.S. High Yield Index and shows that the convertible market’s upside capture is similar to that of CCC rated bonds. Studying the declining periods of higher quality high yield bonds, it’s clear the convertible market exhibits notably less downside risk, further strengthening the case for utilizing convertibles in lieu of CCC rated bonds.

Data 01/01/97 to 05/31/26. Source: FactSet, ICE Data Services, Voya IM. Convertibles: ICE BofA U.S. Convertibles Index. BB-B/CCC bonds: ICE BofA U.S. High Yield (BB-B) Index and CCC & Lower Index. See endnotes for index definitions.

Implementation considerations

What investors should weigh before reallocating: Convertibles typically offer lower stated coupons than CCC rated bonds, so investors should evaluate the tradeoff between current income and total return potential. Performance may also be influenced by equity market volatility, issuer-specific equity sensitivity, and broader “risk-off” conditions. In sharp credit recoveries, lower-quality high yield may rebound more quickly, which can create periods of relative underperformance for convertibles.

Conclusion

A stronger substitute for lower-quality credit risk: Convertible securities offer a significantly higher return, demonstrate lower volatility, and provide greater diversification benefits relative to CCC rated bonds. For high yield mandates seeking to reduce exposure to the weakest segment of the credit market, convertibles may offer a more efficient way to retain upside potential while improving diversification and downside resilience.

A note about risk: All investing involves risks of fluctuating prices and uncertainties of rates of return and yield inherent in investing. All security transactions involve substantial risk of loss. Debt instruments: Debt instruments are subject to greater levels of credit and liquidity risk, may be speculative, and may decline in value due to changes in interest rates or an issuer’s or counterparty’s deterioration or default. Market volatility: The value of the securities in the portfolio may go up or down in response to the prospects of individual companies and/or general economic conditions. Price changes may be short or long term. Local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issue, recessions, or other events could have a significant impact on the portfolio and its investments, including hampering the ability of the portfolio’s manager(s) to invest the portfolio’s assets as intended. Issuer risk: The portfolio will be affected by factors specific to the issuers of securities and other instruments in which the portfolio invests, including actual or perceived changes in the financial condition or business prospects of such issuers. Interest rate risk: The values of debt instruments may rise or fall in response to changes in interest rates, and this risk may be enhanced for securities with longer maturities. Credit risk: If the issuer of a debt instrument fails to pay interest or principal in a timely manner, or negative perceptions exist in the market of the issuer’s ability to make such payments, the price of the security may decline.