Fixed Income Perspectives: Don’t Reach for Yield as Risks Intensify

Head of Multi-Sector Fixed Income

Even as geopolitical uncertainty clouds growth, attractive yields in high-quality fixed income offer durable return and portfolio resilience.

The war in Iran unfolded against a macro backdrop that was constructive, if uneven, as the year began. AI‑driven disruption in the software sector created pressure in parts of the credit market—most notably private credit and senior loans—even as inflation continued to ease from elevated levels, wage growth stayed well‑contained, and the labor market showed ongoing signs of normalization. None of these factors were particularly worrisome on their own, but together they left the economy with a narrower margin for error.

Now, that margin is even tighter. The current growth outlook hinges on trade flow and how quickly shipments through the Strait of Hormuz can resume. If flows resume soon, the economic impact should be limited. More persistent disruptions, however, would meaningfully increase downside risks to growth (Exhibit 1).

Layering a supply-side shock on top of already softening macro conditions raises the likelihood that growth could weaken further. That said, this shock does not redefine our base outlook. Instead, it increases risks to the downside.

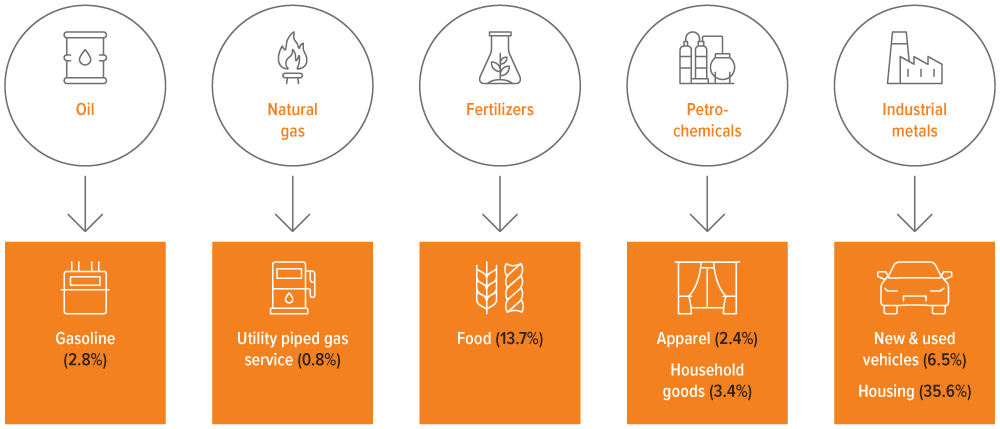

As of 03/11/26. Source: BLS, Voya IM. Data in parenthesis show the percentage of CPI.

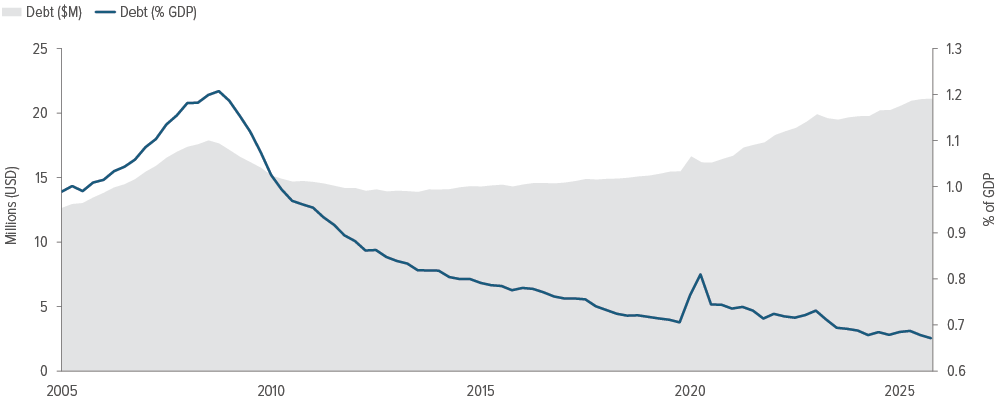

Underneath the geopolitical headlines, concerns about private credit markets continue to percolate, fueling comparisons to past financial crises. While private credit may contribute to volatility or idiosyncratic stress, we do not view this as systemic. Leverage is lower, underwriting quality is stronger, and risk is less concentrated within the banking system than it was in 2007 (Exhibit 2).

As of 10/01/25. Source: Board of Governors of the Federal Reserve System, U.S. Bureau of Economic Analysis, St. Louis Fed. Data shown 01/01/05-10/01/25.

The conflict in Iran adds a significant new layer of uncertainty, complicating the Federal Reserve’s policy outlook and constraining its ability to cut rates even as growth risks increase. At the start of the year, our base case anticipated two rate cuts beginning mid‑year. Based on current conditions, we now expect any easing to be pushed out until uncertainty subsides. As a result, rates are likely to remain higher for longer, with price stability outweighing growth concerns in the near term.

Implications for client portfolios

- Income matters more than timing in an environment of resilient growth but heightened uncertainty.

- Investors don’t need to reach for risk when elevated yields are readily available in high quality fixed income sectors.

- Securitized credit and higher quality segments continue to offer relative value against a volatile macro backdrop. By contrast, we’re more cautious toward emerging markets that are net energy importers.

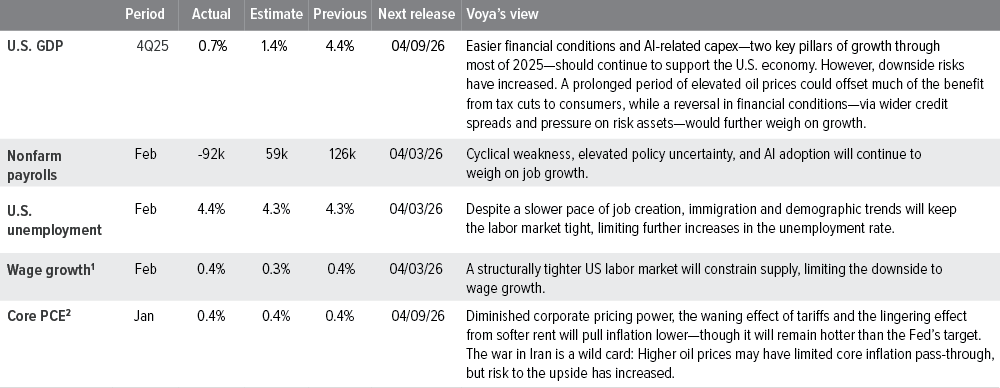

As of 02/23/26. Source: Bloomberg, FactSet, Voya IM.

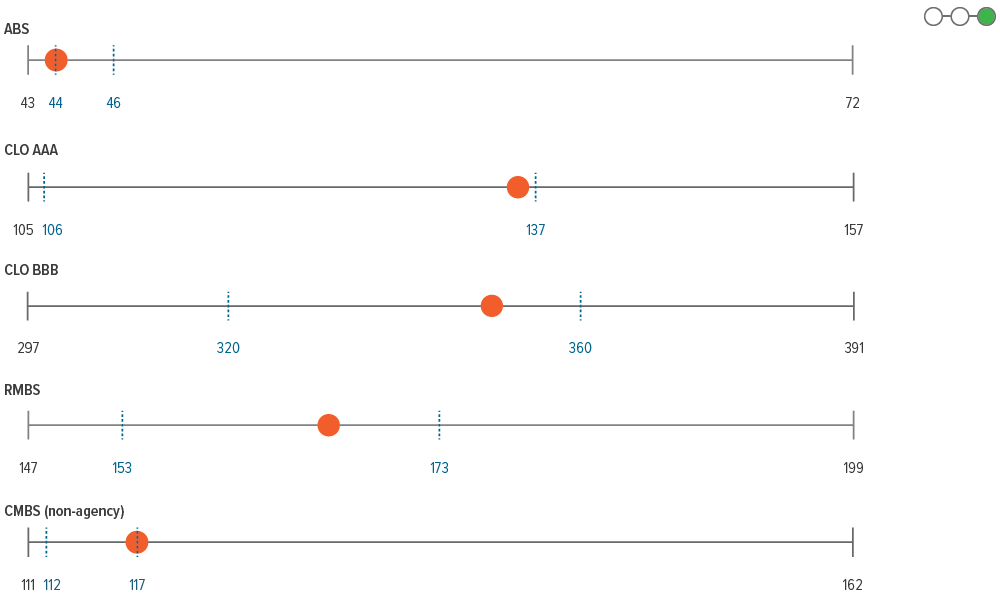

As of 02/28/26. Sources: Bloomberg, J.P. Morgan, FactSet, Voya IM. See disclosures for more information about indexes. Past performance is no guarantee of future results.

Sector outlooks

- Spreads have widened primarily due to heavy supply, not geopolitics, creating selective value in high quality issuers despite ongoing volatility.

- Demand from yield oriented buyers (insurance, life mandates) remains a stabilizing force as yields approach attractive absolute levels.

- 4Q25 earnings were strong, as expected, with fundamentals continuing to look supportive for IG spreads.

- Allocations should focus on the belly of the risk curve.

- Performance has been pressured by rate volatility and supply, with BB rated bonds underperforming after starting the year at very tight levels.

- Despite geopolitical risk, there has been no disorderly sell off, reflecting persistent cash on the sidelines and reluctance to de risk aggressively.

- Loan markets have stabilized and retraced recent losses, supported by firming technicals and demand from CLOs.

- AI related and software exposed issuers are showing relative resilience, with disruption risks increasingly differentiated at the issuer level.

- Risks to watch: increased possibility of policy error, price discovery challenges related to AI developments, and ongoing geopolitical events that could shift inflation and monetary policy expectations.

- Recent underperformance has been heavily influenced by rate volatility, technical factors, and policy news.

- While spreads remain tight, recent underperformance supports a more neutral view on agency MBS, particularly as a ballast in multi sector portfolios amid an uncertain macro backdrop.

- Overall, fundamentals and the supply technical should be a positive influence on mortgage returns going forward.

- CLOs have partially rebounded after a dislocation early in the month, tracking stabilization in the loan market and renewed investor demand.

- While CMBS demand remains strong, robust new‑issue supply has created a more nuanced technical backdrop.

- While relative value in securitized credit remains, recent resilience across most sectors points incremental allocations toward other areas offering more compelling tactical opportunities.

- A weaker U.S. dollar should support continued inflows in EM assets, particularly higher-yielding local bonds.

- Hard currency EM spreads have shown remarkable resilience, with limited pricing of a prolonged Middle East conflict.

- Most repricing has occurred in local markets, driven by sharp shifts in global rate expectations and reduced central bank cut pricing.