Jeffrey Hobbs, CFA

Head of Insurance Portfolio Management

Key Takeaways

Higher rate volatility and a wider range of forward paths mean investors must consider potential shocks when constructing portfolios.

The road forward depends on how you got here in the first place and the unique circumstances of your balance sheet.

We highlight opportunities ahead for 12 asset classes through the lens of an insurance investor.

…and I—I took several roads at once, based on the specific needs of my balance sheet, and that has made all the difference.

When you come to a fork in the road, take it

Robert Frost is strolling in the woods when the road splits in two. After much contemplation, and lacking the technology to clone himself, he takes the “one less traveled by” with a bit of self-satisfaction and a tinge of second-guessing.

We insurance portfolio managers have easier choices. We don’t build portfolios for just one future path of the economy, but rather for a probabilistic set of future outcomes. We can take two (or more!) roads at once as we forge a path that delivers on our investment objectives—weighing new information and tilting the portfolio in ways we believe will deliver attractive through-the-cycle returns for our levered balance sheets.

For the longest time, we lived with a Federal Reserve that relied heavily on forward guidance, which shaped the market’s view of the path ahead. Now, the Fed is necessarily data dependent, leading to higher rate volatility and a greater range of outcomes. Recent economic data has reinforced the base case of easing inflationary pressures, driven by slower consumer spending, tighter credit standards and higher borrowing costs. Yet exogenous shocks, such as higher energy prices or emboldened labor negotiatiors from Hollywood to Motown, can still influence the path for inflation, while stress in lending markets can hasten an economic slowdown. The soft-landing scenario increasingly priced into the market could readily branch off at any moment on a different course.

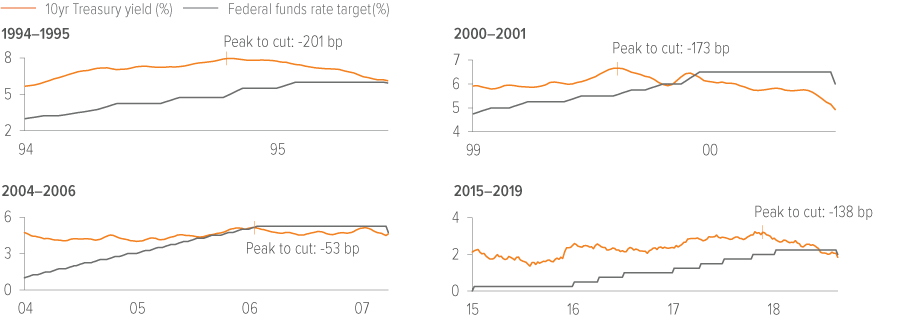

Because insurance company balance sheets are unique and require customized approaches, it matters how you got to this point on the path when considering next steps. For those of us who manage proprietary assets, we are rarely starting a new journey, so moving forward depends on how the portfolio is constructed. For much of 2022, our allocation to duration was more barbelled—over-indexed to floating-rate assets at the front end, adding spread duration out the curve opportunistically. With investable yields once again approaching local highs, we lean toward extending duration in portfolio accounts that have adequate liquidity and room in their asset/liability duration bands. Consider: during the last four rate-hike cycles, the 10-year Treasury yield peaked before the final rate increase and well before the first cut (Exhibit 1).

For some P&C and health companies, staying shorter duration and more liquid has been the right decision so far. But the path forward may be to go more barbelled, moving some excess liquidity and floating-rate assets out to the 10-year part of the curve. It’s been a hard ask for short-duration fixed income investors to move even into the belly of the curve given the size of the yield curve inversion. But adding high-quality duration can provide a portfolio ballast for those darker future economic paths.

Although higher rates mean that investable yield is now driven more by the rate component than the spread component, how you position across spread sectors will still drive a meaningful part of your performance over a business cycle. Life insurance investors, for example, can attribute most of their distributable cash flow to spread income.

As of 09/30/23. Source: Bloomberg Index Services Limited, Federal Reserve, Voya IM.

An insurance lens on asset class opportunities

Like Frost, who “looked down one as far as [he] could,” we offer brief asset class views below, providing a glimpse down a covered path.

Investment grade (IG) public credit

IG spreads are below historical averages at a time when the economy is slowing. However, we see spread levels as fair given solid fundamentals and attractive all-in yields. A meaningful slowdown in long-duration issuance amidst the recent rise in rates has offered technical support to this part of the market.

Investment grade (IG) private credit

The more domestic-focused, insurance-heavy, liquidity-constrained IG private placement buyer base has seen spreads widen in 2023 versus similarly rated public comparables. While we often think of spread-to-publics as pro-cyclical—in other words, tightening (or widening) as overall credit spreads tighten (or widen)—spreads over publics have increased this year even as overall public spreads have narrowed. As liquidity becomes more scarce, investors are paid a premium for it.

Below investment grade (BIG) public credit

This year is tracking to continue a four-decade trend in which the broader high yield corporate bond market has never lost money in back-to-back years. Index yields in the high 8s indicate a strong likelihood of positive returns 12 months forward. That being said, very high-quality, short-duration, investment grade fixed income is also likely to deliver positive returns over that same horizon. Current positioning of accounts will influence how much additional spread and carry to add, weighed against the potential for higher volatility.

Below investment grade (BIG) private credit

Middle market strategies have expanded significantly with the prolonged ZIRP environment. Cash flows and coverage levels could deteriorate in a higher-for-longer rate scenario, putting an emphasis on recovery. Cycle-tested managers with deep workout experience, who focus on multiple ways to a par outcome, should outperform in a market that will see increasing performance dispersion.

Emerging market credit

Higher energy prices and global supply chains shifting away from China will create winners and losers. Throw in unsynchronized monetary policy and pockets of elevated political risk, and you get a wide range of heterogeneous opportunities in an asset class that’s often unfairly lumped together.

Agency mortgage-backed securities (MBS)

A lot of favorable trends are taking shape for MBS: attractive spreads on an absolute and relative basis, the conclusion of FDIC liquidations (knock on a New England birch), weakening seasonals, and the twilight of the hiking cycle. In the wake of Covid, the yield-to-worst on the MBS index started with a 0; now, Fannie 6s trade at a discount.1 For insurers looking for high-quality liquid assets or contingent liquidity via the FHLB system, agency MBS has become increasingly attractive.

Mortgage credit

Accumulated home price appreciation and tight housing supply continue to support residential credit Our high-performing, long-standing overweight in seasoned floating-rate agency credit risk transfer securities has been largely tendered away, as CRTs have de-levered so much (and home prices have risen so much) that they now offer little risk relief to the GSEs.

Mortgage derivatives

Interest-only securities offer attractive, high-single-digit unlevered yields to the market’s base-case prepayment expectation. With underlying collateral significantly out of the money to refinance, prepayment risk is low, creating attractive risk-adjusted returns. These securities could see significant spread tightening amid limited new supply, offering compelling risk- and capital-adjusted yield for insurance companies willing to own securities carried at fair value.

Collateralized loan obligations (CLOs)

Rising floating rates and benign default losses have kept CLOs in favor for insurance companies. We expect tranches rated A or better to remain capital efficient in the evolving regulatory framework and loss-remote, despite a weakening medium-term outlook for lower-rated tranches, which are more levered to their underlying collateral.

Asset-backed securities (ABS)

High-quality short spread duration offered across several subsectors has provided attractive diversifying spread premia for insurers.

Commercial mortgage-backed securities (CMBS)

CMBS have the widest dispersion of outcomes within investment grade fixed income. Sub-portfolios can be built in senior single-asset, single-borrower CMBS and commercial real estate CLO securities that minimize office collateral while offering attractive return targets. Seasoned CMBS with long performance histories, large amounts of defeased loans, and a past Covid stress test can allow experienced managers to glean attractive spreads with cushion in credit outcomes.

Commercial mortgage loans (CMLs)

Although falling transaction volume has decreased new loan originations, future refinancings will require additional capital that should be afforded attractive economics with solid downside protection. Continued retrenchment in bank lending is creating opportunities for non-bank lenders, including insurance companies willing to up their allocations. We may be approaching peak bearishness in office; other asset subtypes have valuations above pre-Covid levels, but fundamentals are weakening.

“The Road Not Taken” is often read as an inspirational calling to live life on your own terms, daring to go where others haven’t. However, the diverging roads in the poem are actually not that different. “Both that morning equally lay in leaves no step had trodden black.” Fortunately, there is no need for insurance investors to forge into uncharted territory when constructing portfolios.

Today’s market offers attractive opportunities to drive risk-adjusted income for insurance portfolios. Each marginal decision—on rate positioning and on credit—must take into account the paths that came before. We would be happy to walk the path beside you and share our experience along the way.

|

A note about risk The principal risks are generally those attributable to bond investing. All investments in bonds are subject to market risks as well as issuer, credit, prepayment, extension, and other risks. The value of an investment is not guaranteed and will fluctuate. Market risk is the risk that securities may decline in value due to factors affecting the securities markets or particular industries. Bonds have fixed principal and return if held to maturity, but may fluctuate in the interim. Generally, when interest rates rise, bond prices fall. Bonds with longer maturities tend to be more-sensitive to changes in interest rates. Issuer risk is the risk that the value of a security may decline for reasons specific to the issuer, such as changes in its financial condition. High-Yield Securities, or “junk bonds”, are rated lower than investment-grade bonds because there is a greater possibility that the issuer may be unable to make interest and principal payments on those securities. Foreign investing does pose special risks, including currency fluctuation, economic and political risks not found in investments that are solely domestic. Emerging market securities may be especially volatile. Investments in Mortgage-Related Securities involve exposure to prepayment and extension risks greater than investments in other fixed-income securities. The strategy may use Derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses and have a potentially large impact on performance. Investments in commercial mortgages involve significant risks, which include certain consequences that may result from, among other factors, borrower defaults, fluctuations in interest rates, declines in real estate values, declines in local rental or occupancy rates, changing conditions in the mortgage market, and other exogenous economic variables. All security transactions involve substantial risk of loss. The strategy will invest in illiquid securities and derivatives and may employ a variety of investment techniques, such as using leverage and concentrating primarily in commercial mortgage sectors, each of which involves special investment and risk considerations. Other risks include but are not limited to: Credit Risks; Credit Default Swaps; Currency; Interest in Loans; Liquidity; Other Investment Companies’ Risks; Price Volatility Risks; Inability to Sell Securities Risks; U.S. Government Securities and Obligations; Sovereign Debt; and Securities Lending Risks. |