Mohamed Basma, CFA

Managing Director, Head of Leveraged Credit

Weekly Notables

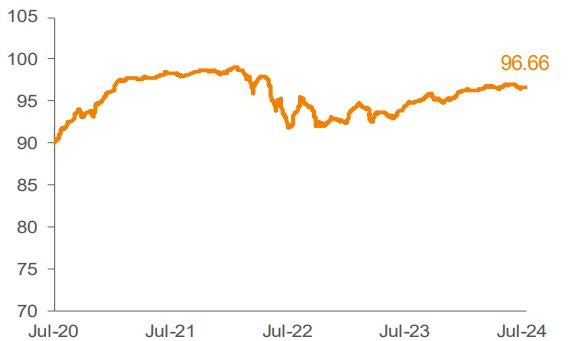

Though the macro tape was relatively light this week, Treasury yields fluctuated following stronger-than-expected retail sales data, mixed commentary from Fed officials and growing political uncertainty around President Biden’s reelection campaign. Equities lost their recent momentum in a volatile trading week, while the loan market remained mostly insulated from the noise, as the Morningstar LSTA US Leveraged Loan Index (Index) delivered a steady gain of 0.19% for the seven-day period ended July 18. Secondary trading levels moved modestly lower, as the average bid price of the Index declined by two bps, closing out the week at 96.66.

Refinancing deals continued to dominate the bulk of primary market activity. While most of the volume replaced existing loans, a few deals refinanced paper out of the private credit market, which has been a prevalent theme this year. Net of anticipated repayments, the amount of net new supply expected to enter the market totals about $1.9 billion, versus repayments outstripping new supply by $44 million last week.

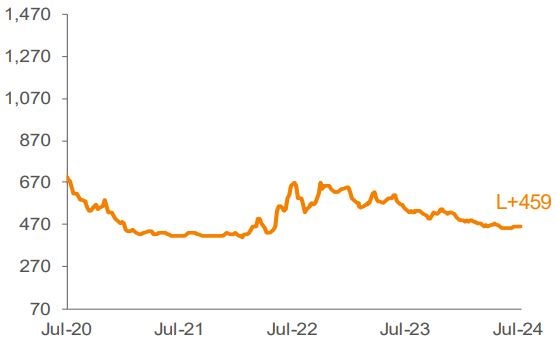

Higher-quality credits performed better over the course of the week, while the riskiest segment of the market experienced some weakness. BBs were up 0.20%, as their average bid of 99.45 gained four bps. Single-Bs returned 0.22%, as their average bid increased three bps, to 98.20. CCCs lost –0.19%, as the average bid across that group fell 35 bps, to 82.53.

CLO managers priced four new transactions this week. YTD issuance is tracking an impressive $106.7 billion. Retail loan funds experienced a net inflow of $634 million, marking a third straight weekly inflow for the asset class.

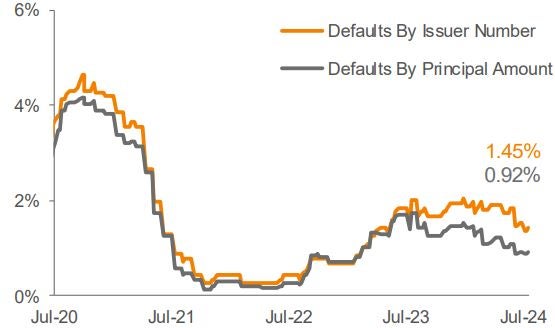

There was one default in the Index this week (Rodan & Fields).

Source: Pitchbook Data, Inc./LCD, Morningstar ® LSTA ® Leveraged Loan Index. Additional footnotes and disclosures on back page. Past performance is no guarantee of future results. Investors cannot invest directly in the Index. *The Index’s average nominal spread calculation includes the benefit of base rate floors (where applicable).