Gregory Michaud

Head of Real Estate Finance

Jason Tessler

Head of Real Estate Credit and Asset Management

Commercial mortgage loans (CMLs) have a track record of strong, differentiated returns that have made them an effective way to diversify institutional fixed income portfolios. Given the historical frictions in CML transactions, many investors assume the asset class is illiquid. However, technologies and platforms to connect buyers and sellers have improved significantly since the 2008 financial crisis. The resulting liquidity has made it easier for institutional investors to access CMLs in a broader range of investment vehicles, including pooled accounts such as collective investment trusts.

Below are answers to commonly asked questions about CMLs and liquidity in the space.

What are commercial mortgage loans?

An investment in CMLs represents whole loans originated directly with companies that own commercial property, such as offices, retail, industrial, apartments, hotel/motel, mixed-use and others. Unlike commercial mortgage-backed security (CMBS) pools, CMLs can be tailored to meet both the demands of the borrower and the lender’s underwriting criteria.

Because of the bespoke nature of CMLs, a comprehensive process of underwriting and due diligence precedes the actual funding. Mortgage underwriting often involves a financial examination of the prospects for the property and the property owner, as well as various third-party assessments, including appraisals, environmental reports and engineering reports. CMLs also require hands-on management after closing. Standard servicing includes collection of updated rent rolls and operating statements, property inspections, and confirmation of paid taxes and insurance premiums.

Are CMLs inherently liquid?

Terms for CMLs vary significantly, allowing investors to tailor an allocation to fit specific objectives. For example, terms for core loans go up to 25 years. Transitional bridge loans have shorter terms that range between 3 and 5 years. In addition, although CMLs are traditionally a “buy-and-hold” asset class, there is a robust secondary market for buying and selling loans across property types.

Which platforms facilitate the sale of CMLs?

Lenders looking to sell a commercial mortgage loan generally have three options:

- Go directly to investors and find a buyer on their own.

- Hire a broker to market and sell the loan on the lender’s behalf.

- Sell the loan through one of the many commercial real estate online auction platforms.

How has the secondary CML market evolved in the past 15 years?

Technology has accelerated the CML review process significantly. In the past, organizing and reviewing the information necessary to evaluate a loan on the secondary market was incredibly inefficient. Commercial loans vary substantially in their underwriting criteria and deal terms, and each loan is accompanied by extensive legal documentation and property information. For example, a loan file may contain thousands of pages of due diligence, such as:

- Loan documentation: Loan agreements, promissory notes and assignment of rents and leases

- Underwriting: Cash flows (historical and pro forma), occupancy history and leases, loan-to-values (LTVs), debt service coverage and debt yield

- Third-party reports: Appraisals, property condition reports, environmental reports, title and surveys

Stacks of paper loan documents had to be converted into spreadsheets before it could be analyzed and reviewed. Furthermore, information was often missing, incomplete and/ or outdated. A potential buyer would need to start with the paper records provided at the time the loan was booked, then go page by page through any new information, which wasn’t necessarily organized and in logical, sequential order. For older loans, the files were often enormous and filled with inaccuracies.

Today, new technologies and customized real estate databases have dramatically streamlined the loan review process. Investors can now review necessary documents in a matter of hours, using digital platforms to complete a process that used to involve several days of reviewing paper files. These improvements, by extension, have led to increased liquidity in the space.

Brokers have become more specialized. In addition to improved technology, brokers now specialize in this area of the market. Previously, traditional mortgage brokers would sell CMLs as a side project. Now, top brokerage firms such as CBRE, JLL and Newmark have dedicated note sale teams with extensive networks of qualified buyers, which makes time to market much faster.

Who are typical buyers of loans in the secondary market?

The introduction of online auction houses has significantly expanded the pool of prospective buyers. These investors are typically high-net-worth individuals or family offices. Since the inception of the online auction platform Ten-X, 52% of properties sold on the site have been bought by out-of-state buyers and 10% have been sold to international buyers. Before these auction platforms existed, CML sales were much more localized, with buyer networks typically constrained to the state or region of each property’s location.

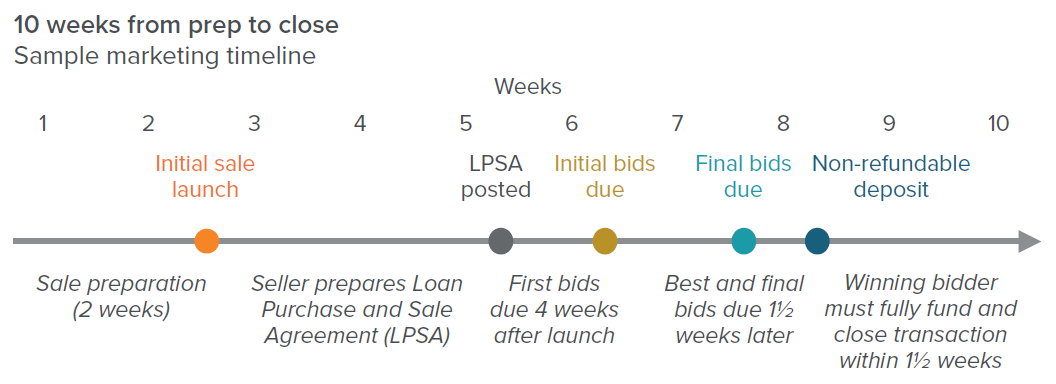

How long does it take to sell a loan?

In our experience, loans sell on the secondary market within four to eight weeks. On the Ten-X platform, 96% of properties have gone from listing to closing within 90 days.1 The timeline below illustrates the sequence of events that precede the sale of a loan.

Are loans sold at a discount?

While sub-performing and non-performing loans have historically sold at a slight discount, the expanded network of prospective buyers has significantly improved price discovery. In addition, selling a sub-performing or non-performing loan is often more cost-effective and efficient than a workout process.

Historically, in stable interest-rate environments, performing loans sell at nearly 100% of their existing value at the time of sale, and many sell at a premium. For example, data from Newmark Knight Frank shows that, in 2019, sales of performing loans ranged from 99% of the loan’s unpaid principal balance (UPB) to above par.

The improved liquidity backdrop for CMLs has provided benefits that go beyond simply managing portfolio cash flows. CML managers are now able to use the secondary market to tactically manage their portfolios—such as selling performing loans to diversify their geographic or borrower exposure, or to take advantage of price increases resulting from spread tightening.

What costs do sellers incur with online auction houses?

Typically, the seller does not pay a fee to post an asset to sell. Compensation for the auction house comes from a buyer's premium of 2–5% of the final bid price.

Has the secondary market remained liquid during periods of volatility?

Yes. As an example, during the period of pandemic-driven volatility, we determined that an online auction would be the best way to maximize recoveries on two non-performing loans. In both cases, recoveries exceeded our expectations. Prior to auction day, we vetted qualified buyers, requiring proof of funds showing their ability to purchase the CML. Parties included local real estate investors, private equity and family offices from coast to coast. The platform’s dashboards, document sharing capabilities, and easy access to market data for the buyer and seller provided transparency and certainty of execution. Prospective buyers were able to download all documents needed to evaluate the CML without having to leave their offices.

On auction day, we watched in real time as each asset received over 15 bids, with two bidders going back and forth near the end of one auction, maximizing our recovery for that non-performing loan. In both cases, the loans closed within 10 business days following the day of the auction.

How should prospective investors view liquidity in the CML space?

We believe the increasingly active secondary market for CMLs adds another attractive element to managing long-term allocations. The attractive risk profile of CMLs may be attributed, in large part, to the loans’ structural advantages, which play out over the course of market cycles. These advantages include direct access to borrowers and the ability to negotiate directly with property owners during periods of volatility, which helps to drive the workout and recovery process.

For a deeper discussion about how to implement CMLs, please contact your Voya IM representative.