Commercial Mortgage Loans: Enhancing Yields with Real Estate Debt

Head of Real Estate Finance

Key Takeaways

A falling-rate environment can introduce significant reinvestment risk and price volatility into public investment grade fixed income portfolios.

Commercial mortgage loans have historically offered attractive real returns with less volatility than market-traded securities.

The commercial real estate market is experiencing strong transaction and origination volume as well as notable asset price stabilization.

In falling-rate environments, commercial mortgage loans can potentially improve returns—while mitigating portfolio volatility.

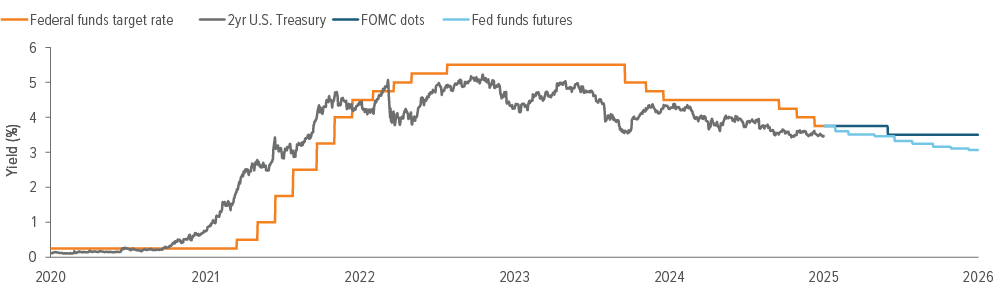

The era of falling yields

Barring a major shift in the macroeconomic outlook, the United States is likely to see sustained declines in interest rates as the Fed normalizes its monetary policy (Exhibit 1). Further, a softening job market could lead to more aggressive rate cuts and falling long bond yields as investors seek safety.

As of 12/31/25. Source: Bloomberg.

Unsurprisingly, yields on most fixed income securities have fallen, as the market expects inflation to remain relatively controlled for the foreseeable future. As such, portfolio managers and asset allocators are faced with the potential of declining income across all fixed income assets.

With falling yields come rising bond prices and thus new challenges for reallocation and reinvestment at lower yields. As these portfolio management challenges are likely to persist, now is the time to consider increasing allocations to real estate debt within a diversified mixed-asset portfolio to maintain sufficient income to meet portfolio obligations.

Commercial mortgage loans have historically offered attractive real returns with less volatility than market-traded securities; this might be especially useful in managing risk-adjusted portfolio returns in coming years.

Looking for stable returns in a potentially volatile market

Market volatility, regardless of explanation, has historically led investors to seek out Treasury and other fixed income securities of all durations, thus lowering yields across the curve.

With the S&P 500’s cyclically adjusted price to earnings ratio sitting near 40 (compared with a 30-year average of 28.5), it is rational to expect investors to seek out bonds for diversification and risk management, irrespective of any fundamental belief on the future direction of equity prices.1

Of note, assets in money market funds (essentially overnight debt investments open to all investors) have nearly doubled since the onset of the pandemic, to $7.8 trillion in 3Q25, given their substantially higher yields.

While it is impossible to know where and when—or even if—this capital will be reallocated out of money market funds as yields fall, it is highly probable that some investors will seek out higher yields via longer-duration and higher-risk fixed income investments. The natural result could be market pressures further lowering yields at the long end of the curve.

This could pose a challenge for portfolio managers who rely on fixed income returns to cover portfolio liabilities, as they may no longer be able to count on near-risk-free overnight rates of return. As a result, managing reinvestment risk—the process of reinvesting into lower-yielding fixed income assets because of maturities and/or portfolio rebalancing mandates— could be significantly more challenging.

Real estate debt—specifically, core investment grade commercial mortgage loans secured by commercial or multi-family real estate assets—could be an excellent home for capital seeking higher income with relative safety and low volatility.

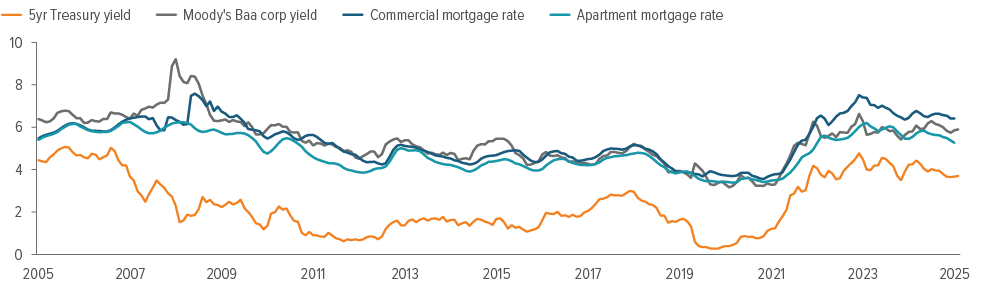

Multi-family and commercial mortgage rates remain more stable than underlying Treasury yields, which are subject to various market forces and more directly tied to the actions of the Federal Reserve (Exhibit 2).

As of 2/17/26. Source: Moody’s, MSCI Real Capital Analytics, Federal Reserve.

The current nature of market volatility, economic uncertainty, geopolitical uncertainty, and even unique factors like the rise of AI all could conceivably lead to greater volatility in equity markets and Treasury yields in 2026 and beyond.

On a relative basis, investment grade real estate debt is likely to provide stable returns based on real assets that can hedge inflation and be underwritten based on property market fundamentals.

The relatively higher rates on mortgage debt have generally subdued new supply and thus created even greater stability in existing real estate assets and real estate debt investments. Thus, real estate debt is an asset class that can potentially provide a natural hedge against overall volatility while still offering a meaningful risk-adjusted real return.

However, two major idiosyncratic risks remain.

The first is continued monetary and fiscal policy uncertainty; the actions of federal policymakers could (and should!) have major implications on the U.S. economy and the interest rate environment. What Congress, the courts, and the president will do is beyond speculation, but the funding of major social spending priorities and tariff policy are not likely to be settled anytime soon.

Second, business enterprises of all sizes are being forced to adapt rapidly to new technologies driven by artificial intelligence; this creates many new downside risks and upside opportunities across practically every industry in the world.

One popular playbook during times of rapid technological change calls for investors to seek out real assets—including fixed income instruments secured on real assets—for their perceived safety and ability to deliver reliable returns amid overall volatility.

Commercial real estate performance in focus

The last several years have been challenging for the real estate asset sector. Higher interest rates caused a reduction in transaction volume, and prices declined from peaks reached in the 2021 post-Covid reopening boom.

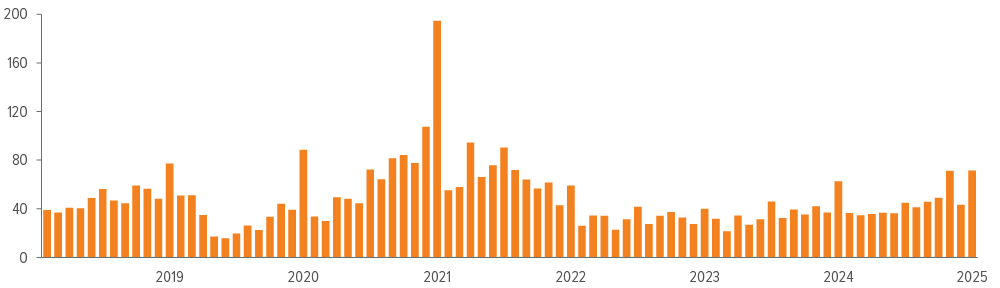

Thankfully, the data now suggest an effective total market turnaround, with sustained price growth and increases in transaction volume (Exhibit 3). According to MSCI Real Capital Analytics data, transaction volume is up 17% year over year for both 3Q25 and yearto-date 2025, with single asset sales (which exclude portfolio and entity transactions) up 26% over both periods.

As of 2/17/26. Source: MSCI Real Capital Analytics.

Further, the RCA Commercial Property Price Index (CPPI) is now trending up, with a 2.6% one-year gain (2.2% quarterly change). Overall, market sentiment in the commercial real estate industry is positive given the overall level of asset stability and now falling interest rates; many expect continued improvement in pricing for 2026.

As shown in Exhibit 3, transaction volume appears to be more or less normal for 2024 and 2025, when compared with historical data. Fears of massive waves of default in commercial and multi-family mortgages have largely failed to materialize, and even in regional and national banks with exposure to large, commodity office towers, NPL ratios remain below 2%.3

With the downward trend in interest rates now underway, it is rational to believe most of the worst-case scenarios discussed in prior years are unlikely to come to pass. As such, institutional real estate investments (including real estate debt) are poised to perform well in the coming years and could even provide relative safety and outperformance in many macro downside scenarios.

Given that construction starts have been lower for almost all real estate sectors, long-term supply and demand dynamics are likely to be favorable to owners and lenders for the foreseeable future. Even with lower interest rates, the challenges in construction pricing, lack of labor availability, and strict local market regulations (i.e., zoning challenges) are all likely to reduce the risk of overbuilding for the foreseeable future in most major markets.

With the likely continuation of gains in real estate transactions, as well as the continued stabilization of asset prices and potentially lower underlying interest rates, there is likely to be increased demand for commercial mortgages from borrowers seeking to refinance and/or transact.

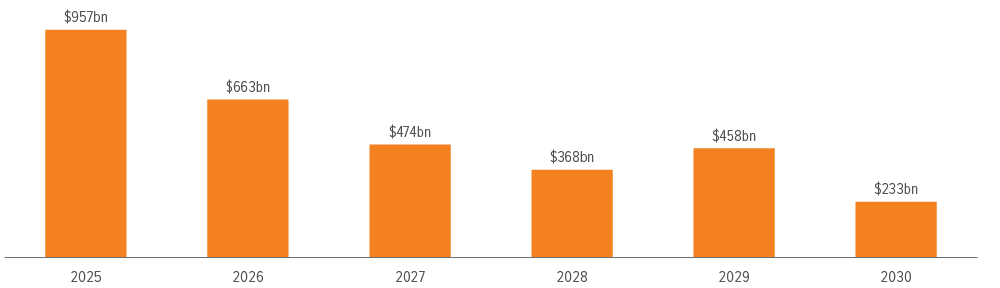

The known wall of maturities—loans that have come due but not yet refinanced—will likely produce opportunities for new loan origination at relatively favorable spreads and pricing to the lender (Exhibit 4). Thus, investors in real estate debt should be able to gain exposure to high-quality loans at relatively attractive returns in 2026 and beyond.

As of 10/31/25. Source: Mortgage Bankers Association, Voya IM.

Looking onward into 2026, a significant potential risk factor would be any reignition of higher rates of inflation. Tariffs, labor shortages due to tighter immigration policy, and even higher electricity costs due to data center demands all could lead to unexpected spikes in inflation in 2026.

If this occurs, real estate asset returns could be impacted by rising costs, at least in areas where pricing power does not allow for rent increases. On a relative basis, real estate debt is less impacted at the asset/operational level, but it is more exposed to declines in real returns (meaning impact due to inflation itself); thus, floating-rate structures may prove attractive to debt investors for the short term to naturally hedge such risks.

The challenges of managing a diversified portfolio in a falling-rate environment

While falling rates are generally considered positive for the economy, the business sector, and consumers, they can pose particular challenges to portfolio managers attempting to construct and maintain risk-balanced, mixed-asset portfolios.

First, stock market returns have historically been quite volatile over periods of declining interest rates. (Think back to 2001 and the 2007-2008 period.) This is easily understandable, given that falling rates are often associated with flights to safety and the Fed loosening monetary policy to stimulate the economy.

Second, fixed income assets can become more volatile due to fluctuations in interest rates (and thus prices), as maturing debt investments need to be reinvested at lower yields.

Thus, deciding what fixed income assets to buy can be more challenging in such times than during periods of stable interest rates. In recent years, high yields on short-term Treasuries made getting current yield relatively easy, but that option is quite likely to disappear over the coming year(s). As such, a search for yield will likely become a major factor in portfolio allocation and asset selection.

We fundamentally believe real estate assets, and specifically commercial real estate debt, deserve consideration for higher allocations in these environments. Core commercial mortgage loans can provide stable yields with potentially better risk-adjusted returns than traditional investment grade fixed income assets such as Treasuries and corporate bonds alone.

Given that real estate debt yields are driven by the rents generated on the underlying assets, they offer inherent diversification from many risk factors impacting stock market equities and corporate bonds. Thus, increasing commercial mortgage loan allocations could be prudent for not only real income enhancement but also fundamental risk diversification.

Written in partnership with Joshua Harris, PhD, CRE, CCIM, CAIA, Economist, Lakemont Group.

A note about risk

All investing involves risks of fluctuating prices and uncertainties of rates of return and yield. Investments in commercial mortgages involve significant risks, which include certain consequences as a result of, among other factors, borrower defaults, fluctuations in interest rates, declines in real estate values, declines in local rental or occupancy rates, changing conditions in the mortgage market, and other exogenous economic variables.

All security transactions involve substantial risk of loss. The strategy will invest in illiquid securities and derivatives and may employ a variety of investment techniques, such as using leverage and concentrating primarily in commercial mortgage sectors, each of which involves special investment and risk considerations.