Jeffrey Hobbs, CFA

Head of Insurance Portfolio Management

Higher investible yields and elevated volatility have combined to create meaningful opportunities for insurance companies with the willingness and ability to capitalize.

Highlights

- After the historic bond market selloff in 2022, we believe there are ample opportunities to improve risk-adjusted returns and income.

- With current investible market yields above portfolio book yields, portfolio turnover can help insurers increase book yields — a sharp reversal from the conditioned behavior of the last decade.

- Nimble portfolio positioning must balance higher investible yields against the evolving economic backdrop and financial statement constraints.

Mick Jagger once crooned, “You can’t always get what you want. But if you try sometimes, well, you just might find, you get what you need.”

If surveyed at the start of 2022, most insurance market participants would have said that 5–6% yields on investment grade instruments would satisfy liabilities and drive profitability. In other words, the insurance industry needed higher investible yields to improve profitability. On the other hand, the industry sure did not want the abruptness of the move to get there.

As of 12/31/22. Source: Bloomberg. Investors cannot invest directly in an index. Past performance does not guarantee future results.

Gimme shelter?

It’s time to move past the bunker mentality of 2022 and take advantage of the broad opportunity set to improve risk-adjusted returns and income.

Higher rates, wider spreads and falling equity values made for widespread negative total returns in 2022. Indeed, the recent market rout forced many insurers into a bunker mentality. Investment activity slowed due to lower operating flows, management or board-level risk concerns, and/or financial statement constraints around realizing losses.

In hindsight, investors should have avoided this bunker mentality. Amid the market carnage, investible yields rose to decade-plus highs, and the improved opportunity set in 2022 would have allowed investors to increase portfolio yields while creating modest risk headroom.

If they haven’t already, we urge insurers to emerge from their bunkers and look around. We expect interest rate volatility will continue to recede as central banks move beyond peak hawkishness. However, rates should linger at higher levels, creating ample opportunities to improve risk-adjusted returns and income.

Buoyed by higher fixed income earnings, historically positive ratings migration, and limited defaults, 2022 was a bumper year for capital generation. Looking ahead, default rates are likely to remain subdued in the first half of 2023. At a minimum, ratings migration should slowly turn from a decided tailwind to a modest headwind.

Paint it black

After so much red in 2022, return scorecards may very well be painted black in 2023, with high probabilities for shorter-duration products.

Of course, the bunker mentality of 2022 was not completely unjustified. One year in the red is bad enough, and risk certainly remains elevated. The good news for insurers is that markets will likely pivot from pricing interest rate risk to pricing fundamental risk. This is fertile ground for insurers to pick and choose where they take risk. In our view, high yields on short-duration assets and wide spreads on floating rate pan-securitized credit provide attractive carry with limited risk of a negative calendar-year total return.

Even further out on the credit curve, high yield corporate bonds have never faced negative total returns for consecutive calendar years. In addition, the carry in the asset class and discount dollar prices make negative returns for high yield less likely in 2023.

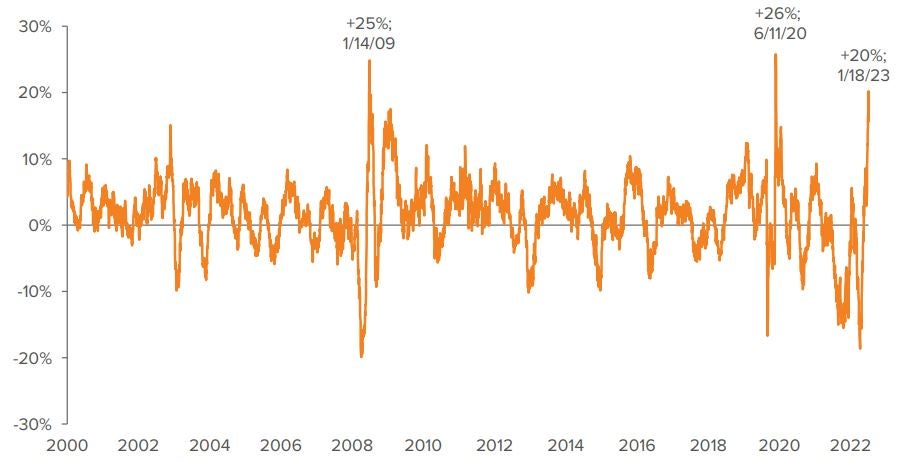

Get off of my cloud

If you need proof of the benefits of nimble portfolio positioning and taking calculated risk during market dislocation, look no further than long corporate bonds.

Bond heaven is a rare and special place. As fixed income investors, we live in a world where there can be asymmetric downside to the netherworld. In 2022, amid historically poor fixed income returns, the Bloomberg Barclays Long Corporate Index ended the year on one of its strongest runs on record. That might seem remarkable to some readers given the dramatic selloff experienced in fixed income for the bulk of last year.

As of 01/18/23. Source: Bloomberg. Investors cannot invest directly in an index. Past performance does not guarantee future results.

Low-coupon, long-duration securities issued in recent years created opportunities to purchase very low-dollar-price, positively convex securities during the selloff, as the Bloomberg Barclays Long Corporate Index troughed at just 75% of par. Very high realized volatility provided tactical opportunities to purchase discount securities. As rates and spreads rallied back sharply, securities purchased at this time drove sizeable trading gains late in the calendar year. For more book-focused investors, this created gains that could be used to offset losses and increase portfolio book yields in other parts of the portfolio. High realized volatility can be a feature of long-duration asset classes and not just a bug.

Start me up

With investible market yields routinely above book yields, portfolio turnover is no longer the enemy.

When investible market yields were persistently below portfolio book yields in the post– financial crisis era, many insurance companies responded by slowing down portfolio turnover to protect book yields. With current investible market yields above portfolio book yields, portfolio turnover can now help insurers increase book yields — a sharp reversal from the conditioned behavior of the last decade.

Exhibit 3 shows a trailing 15-year history of the coupon and yield-to-worst of the investment grade corporate bond index. The sharp increase of market yields (gray line) above coupons (orange line) signals that there is meaningful opportunity to increase book yields. There are opportunities to add yield into portfolios, but, of course, we want to do it in a risk- and capital-aware manner. Against an uncertain economic backdrop, there is a broader set of potential outcomes, making it important (as always) to be mindful of the impact of realized losses on GAAP and STAT balance sheets.

As of 1/30/23. Source: Bloomberg. Investors cannot invest directly in an index. Past performance does not guarantee future results.

Time is on my side

Investment grade private credit and commercial mortgage loans are a strong match for long-term-minded insurance investors.

Many insurers extolled the idea of going “up in liquidity” in 2022 as opportunities in public markets improved and some business models faced liquidity pressures. For those able to stay in private markets, spread-to-premiums remained healthy after a brief decompression. Slower demand for private credit and the more challenging financing market allowed lenders to draw attractive covenant packages that should create value over time. Like the cyclicality inherent in markets broadly, spread-to-publics can vacillate as market conditions change and investors are compensated — both in higher upfront spread and back-end fee income as well as higher recoveries — to invest through the cycle.

The resilience of commercial mortgage loans (CMLs) has been on full display since the pandemic-driven economic drawdown. In our own Voya portfolios, CMLs proved durable and experienced close to zero impairments despite the extraordinary disruption to economic activity that began in early 2020. This resiliency should come as no surprise for veterans of the asset class. The CML market is dominated by patient, long-term institutional investors such as insurance companies, pension plans and banks. CMLs continue to offer attractive relative value for insurers. As of early March, coupons for core loans were north of 5%. At this level, a core loan with a 10-year term, 30-year amortization schedule, and 5.75% coupon equated to a 190 basis point spread over the average life treasury. These core loans also offered 80 basis points over an A- rated corporate index, and 95 basis points over the comparable A rated corporate index.1

With strong structural protections and the ability to directly negotiate with property owners during periods of volatility, CMLs are also a compelling way to gain selective exposure to attractive properties in areas of commercial real estate that are facing broader headwinds (see more below).

Beast of burden

SASBs in the industrial, multi-family and life sciences spaces are compelling. Higher-yielding office and retail CMBS aren’t worth the reach … yet.

One of the lasting secular trends of the pandemic will be a fundamental reshaping of the office landscape in commercial real estate. There will be some modest scarring in the insurance industry from office lending done in a different market environment for those assets. For investors with relative underweights to the office subsector (like Voya IM), there may be attractive lending opportunities, over time, as the property sector evolves. In securities form, single asset single borrower (SASB) securities and multi-family-focused CRE CLOs with no office exposure allow nimble investors to gain targeted exposure to the commercial real estate market.

Among SASBs, we prefer property types in the industrial, multi-family and life sciences subsectors. Industrial collateral has benefited from retailers catching up to Amazon, as well as the need for facilities to support “last-mile” distribution as consumer preferences dictate. Multi-family has benefited from demographics in the US, as well as structural underinvestment in housing stock and the resulting growth in rents.

Life sciences collateral is essential, purpose-built laboratory/office space supporting a segment of the economy that cannot work from home. Select properties in the hospitality space are also attractive at current levels. We prefer irreplaceable “trophy” hotels that are benefiting from currently insatiable consumer demand for vacation travel, as well as extended stay–oriented and suite-style hotels that cater to the price-sensitive business traveler. These properties have proven very resilient post Covid.

Tumbling dice

We believe securitized credit offers a range of attractive yields and different flavors of risk, and that it should be a part of any insurer’s allocation.

Other than during the brief pandemic dislocation, high-single-digit yields were generally unavailable for corporate credit investors (outside of the deepest speculative-grade public credits) in recent years. In the current environment, there is widespread opportunity to invest in 6–8% prospective yields across securitized subsectors. In the table below, we list some of our own greatest hits.

Our tactical views on securitized credit

Source: Voya Investment Management.

Troubles a’ comin

For insurers that over-indexed on less liquid securities and structures that provided capital relief, statutory capital pressure could soon be mounting.

After a decade-long start-stop process to refine bond factors in the risk-based capital calculation, the evolution of the insurance regulatory capital regime is newly accelerating. With changes in securitized modeling, a workstream on CLO capital charges, the “definition of a bond” project, and pushback on select structures, a staid industry slow to change is set for rapid transformation. In our evaluation, Voya is looking for structures that drive true risk transformation. Structures that simply drive capital arbitrage or are aimed at reworking financial statement geography appear to be in the crosshairs of the panregulatory bodies.

(I can’t get no) satisfaction

Insurance investors have long clamored for higher investible yields. They arrived with a fury in 2022. Even with a rally back in spreads and rates to end the year, investible index yields are still generally higher than the peak yields reached during the height of pandemic uncertainty in March 2020.

The 2023 market environment offers insurers significant opportunities to drive positive economics for their stakeholders. If you are not getting satisfaction from your manager, we are happy to discuss portfolio solutions for your balance sheet.